Despite valiant surges by bell pepper and cauliflower, the produce industry needs an increase in demand to drive up struggling prices.

Hopefully, as the U.S. moves closer to spring and outdoor dining becomes more viable, pent up desire for foodservice might just become the defibrillator that shocks new life into prices.

Even after growers slowed down harvests, allowing coolers to empty, produce sales staffs are fighting for a few extra dollars to reach breakeven levels on many commodities.

ProduceIQ Index: $0.86 /pound, -1.2 percent over prior week (Week #9, ending March 5th)

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

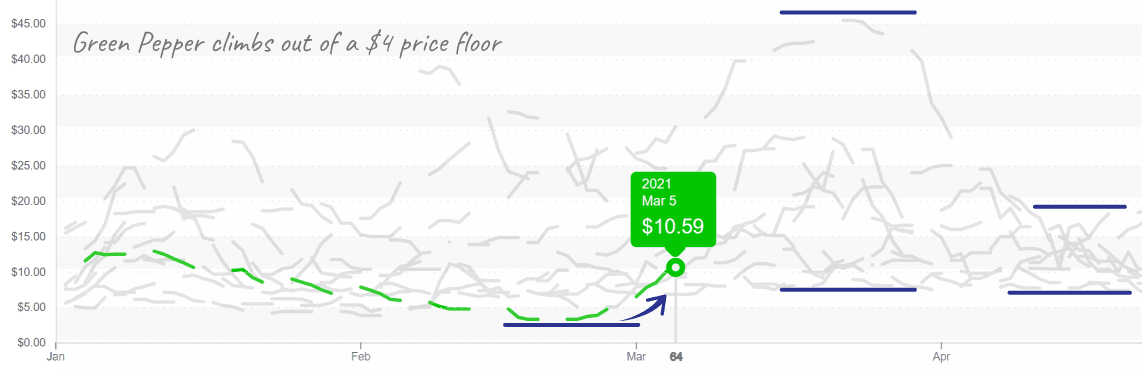

Bell peppers, jumping +73 percent in a week, came off a $4 market and are now nearing prices that reflect the cost of production (higher than $10/case).

A $4 price point resembles the post-harvest variable costs, providing no return to the growing costs and creating significant farm operating losses. Excellent quality and an abundant supply on all grades of bell pepper is expected to continue.

Green Bell Peppers jumped towards a breakeven price level after lingering at the lowest pick & pack level.

Cauliflower is the biggest mover in week #9, gaining +82 percent. This time of year, cauliflower and iceberg lettuce, grown in Yuma AZ, accounts for the majority of movement in the U.S according to USDA data.

As a result of Yuma’s growing season winding down, supply on cauliflower is tightening and market prices are increasing. Iceberg’s movement, on the other hand, is trending above historic averages, and quality remains unaffected by Yuma’s seasonal transition to the Salinas, CA growing region.

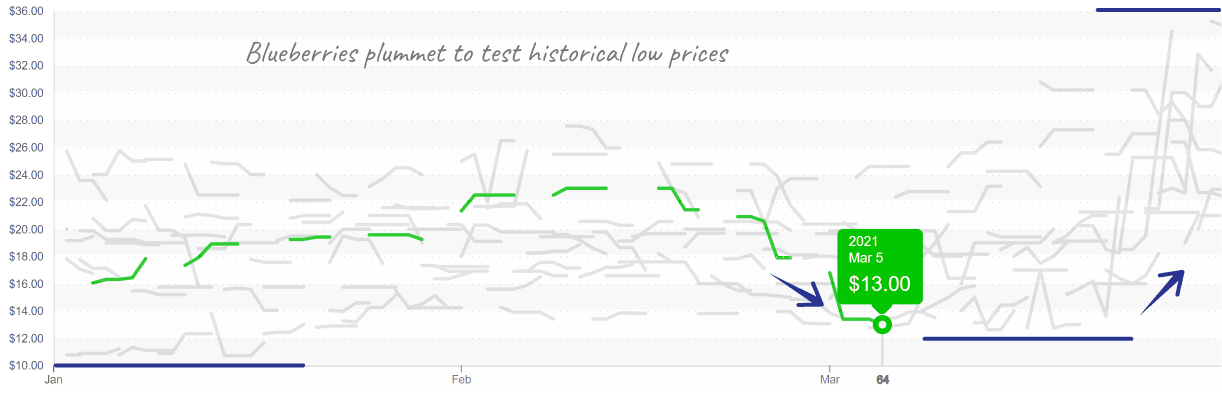

Blueberries and strawberries continue their multi-week decline. Strawberry losses mirror price movements in prior years, falling after Valentine’s day. Strawberries from the golden state are selling at slightly higher prices due to their superior quality over Florida and Texas crops.

Conversely, blueberries set a new historical precedent for this week #9, after a -29 percent decline. Berries are promotable and quality is expected to remain high throughout March.

Dramatic decline in mid-winter blueberry prices compared to prior 10 years.

ProduceIQ Index

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Despite valiant surges by bell pepper and cauliflower, the produce industry needs an increase in demand to drive up struggling prices.

Hopefully, as the U.S. moves closer to spring and outdoor dining becomes more viable, pent up desire for foodservice might just become the defibrillator that shocks new life into prices.

Even after growers slowed down harvests, allowing coolers to empty, produce sales staffs are fighting for a few extra dollars to reach breakeven levels on many commodities.

ProduceIQ Index: $0.86 /pound, -1.2 percent over prior week (Week #9, ending March 5th)

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

Bell peppers, jumping +73 percent in a week, came off a $4 market and are now nearing prices that reflect the cost of production (higher than $10/case).

A $4 price point resembles the post-harvest variable costs, providing no return to the growing costs and creating significant farm operating losses. Excellent quality and an abundant supply on all grades of bell pepper is expected to continue.

Green Bell Peppers jumped towards a breakeven price level after lingering at the lowest pick & pack level.

Cauliflower is the biggest mover in week #9, gaining +82 percent. This time of year, cauliflower and iceberg lettuce, grown in Yuma AZ, accounts for the majority of movement in the U.S according to USDA data.

As a result of Yuma’s growing season winding down, supply on cauliflower is tightening and market prices are increasing. Iceberg’s movement, on the other hand, is trending above historic averages, and quality remains unaffected by Yuma’s seasonal transition to the Salinas, CA growing region.

Blueberries and strawberries continue their multi-week decline. Strawberry losses mirror price movements in prior years, falling after Valentine’s day. Strawberries from the golden state are selling at slightly higher prices due to their superior quality over Florida and Texas crops.

Conversely, blueberries set a new historical precedent for this week #9, after a -29 percent decline. Berries are promotable and quality is expected to remain high throughout March.

Dramatic decline in mid-winter blueberry prices compared to prior 10 years.

ProduceIQ Index

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Mark Campbell was introduced to the fresh produce industry as a lender for Farm Credit. After earning his MBA from Columbia Business School, he spent seven years as CFO for J&J Family of Farms and later served as CFO advisor to several produce growers, shippers and distributors. In this role, Mark saw the impediments that prevent produce growers and buyers to trade with greater access and efficiency. This led him to cofound ProduceIQ.