November sales are dominated by the all important Thanksgiving holiday — one of the largest retail opportunities in produce and many other retail departments. This makes it a hard-to-beat sales occasion any year.

However, throughout October and November, shoppers’ concern over COVID-19 rose along with the number of new cases. This resulted in very different Thanksgiving celebrations versus typical years, with less travel, smaller gatherings and earlier shopping to avoid crowds. Much like seen throughout the year, elevated concern also translated into a greater spending at retail versus foodservice. During the month of November, sales for all food-and-beverage-related items (total edibles) increased 9.3%, which was up from 8.6% during the month of October.

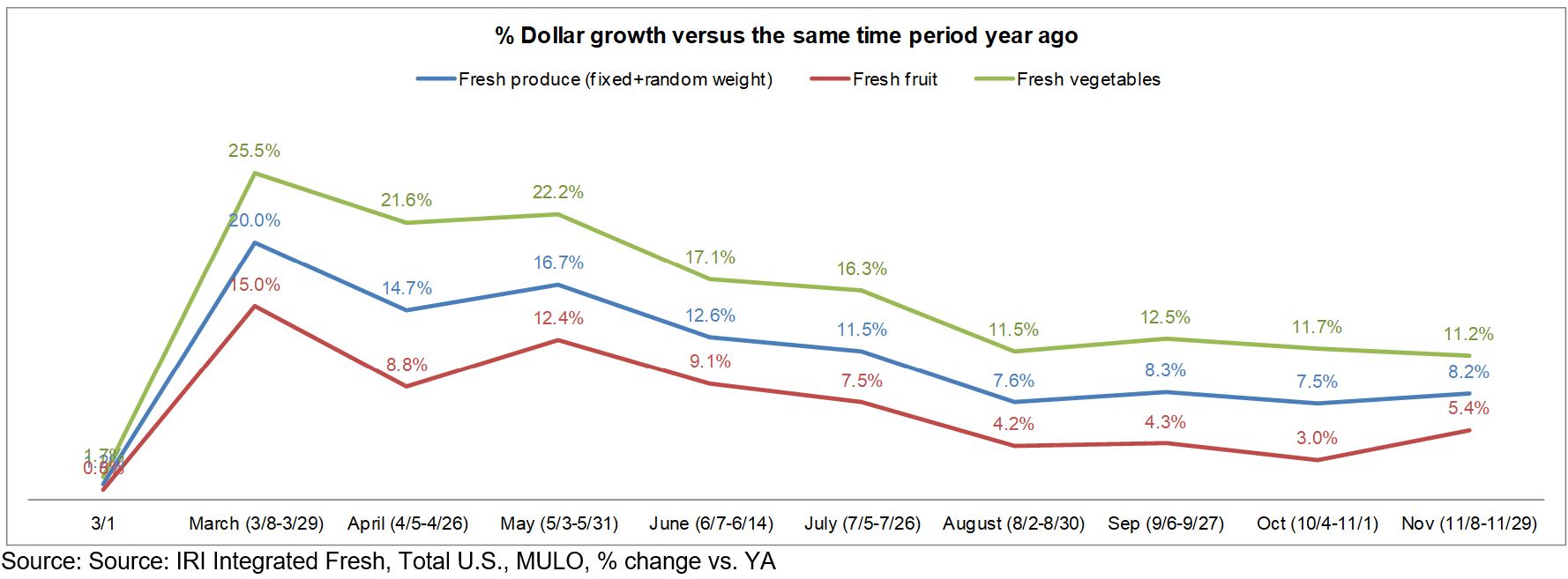

As seen throughout the pandemic, frozen fruits and vegetables have the highest growth, but are also the smallest of the three temperature zones in retail. Frozen fruit and vegetable sales increased 15.6% in November versus year ago versus 8.2% for fresh produce. The 8.2% gain for fresh produce was slightly higher than the 7.5% during the October weeks and gains year-to-date remain unchanged at +10.0% versus the same time period in 2019.

“Retail produce sales delivered a strong performance in November,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “The very different Thanksgiving celebrations benefitted retail, but ultimately balance between retail and foodservice is what benefits our industry as a whole. The end-of-year celebrations are likely to look equally different and looking back at the lessons from Thanksgiving may help streamline operations for the weeks to come. It is likely we will see highly elevated online orders, earlier shopping and different choices to accommodate for the smaller gatherings.”

Fresh produce generated $4.9 billion in sales during the November weeks — an additional $380 million in sales versus the same time period in 2019. This encompasses $107 million in additional fruit sales and $273 million in additional vegetable sales. Vegetable sales have outpaced fruit sales throughout the pandemic and have generated double-digit growth since the onset of the pandemic shopping patterns in mid-March. Fruit did have its best performance since July 2020.

Fresh Share

Looking at total fruit and vegetable dollars in fresh, shelf stable and frozen shows a majority share for fresh, at 76%. While this is below average against the entire 2019 calendar year (84%), this share moves up and down throughout the year. In November 2019, the fresh share of total dollars was 76.6% versus 76.1% in 2020.

“In November, we typically see shelf-stable and frozen coming on strong,” said Jonna Parker, Team Lead for Fresh at IRI. “Perhaps it is the green bean casserole Thanksgiving classic or the lack of fresh summer fruit sales to help boost the produce department. In COVID times, it was actually frozen fruit and vegetables that improved their share from 8.0% in 2019 to 8.5% of total dollars in 2020. Cross-merchandising displays in fresh produce, much like we see integrated displays for all the shelf-stable items for green bean casserole, can be great ways to remind shoppers to of the fresh seasonal classics versus frozen or shelf-stable.”

Fresh Produce Dollars versus Volume

In September, volume sales briefly exceeded dollar sales on aggressive Labor Day pricing. But in October and November, dollar gains once more outpaced volume driven by vegetables.

“Retail fruit sales were perfectly in balance,” said Watson. “Both volume and dollars were up 5.4% in November versus year ago levels. Vegetables had an increase of 11.2% in dollars and 7.5% in volume.”

Absolute Dollar Gains

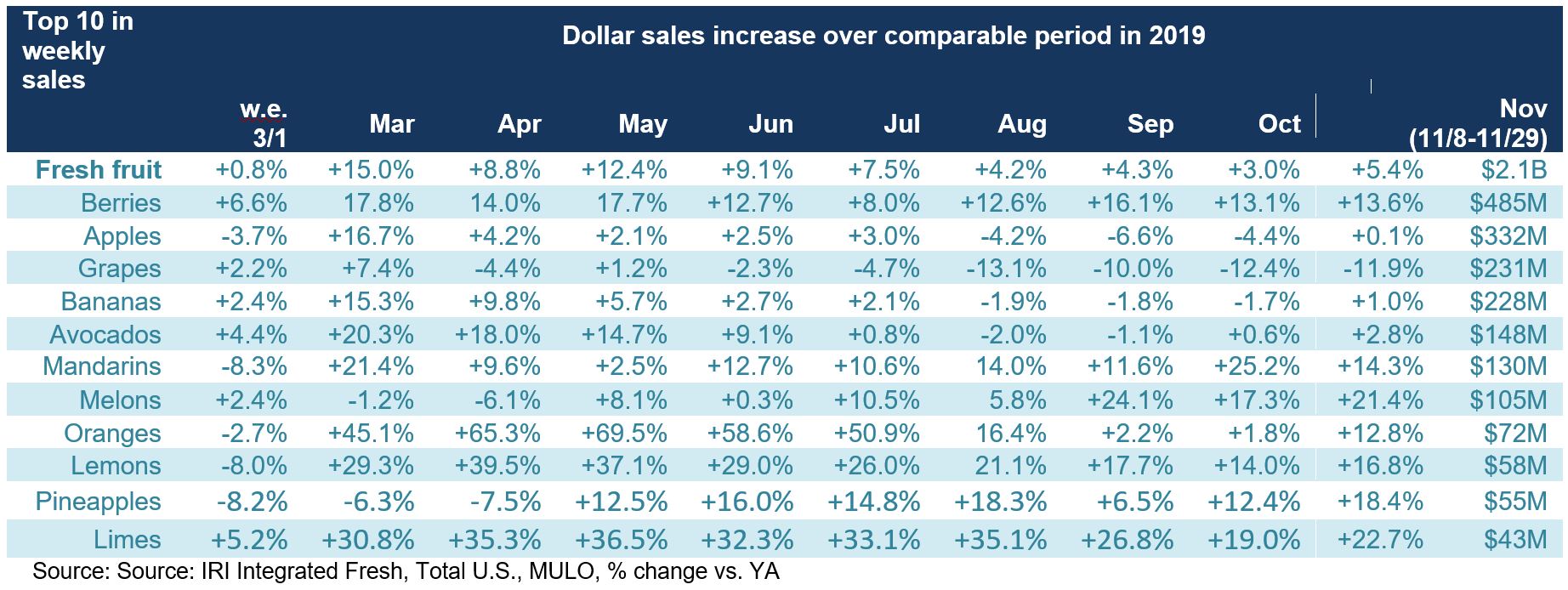

“The November Top 10 in absolute dollar gains reflects some familiar faces, led by berries, tomatoes and lettuce,” said Watson. “Mandarins make an appearance in the top 10 instead of oranges as people’s Vitamin C immune-boosting fruit of choice, with a 14.3% increase versus year ago, reflecting an additional $16.3 million in sales. Cucumbers and mushrooms are the smallest of the categories making it into the top 10, with mushrooms having been a retail powerhouse since March.”

Fresh Fruit

“In fruit, berries remained dominant in sales but the strength of citrus is tremendous,” said Parker. “Citrus fruit is up 14.7% year-over-year in November, the highest of all the areas within fruit. Another area that is doing well is tropical fruit, with a gain of 7.8%, whereas mixed fruit is off 9.5% and stone fruit also fell below last year’s levels in November, at -2.7%.”

Fresh Vegetables

The top 10 in sales on the vegetable side is a strong reflection of Thanksgiving classics.

“Between potatoes, celery for stuffing and sweet potatoes it is clear that shoppers are still thinking about the fresh produce department for their Thanksgiving classics,” said Watson. “The strength of salad kits, lettuce, peppers, etc. is indicative of continued at-home meal preparation and healthful snacking. I believe paying special attention to lunch needs is one of our biggest new sales opportunities with students in virtual schooling and many adults working from home.”

Fresh versus Frozen and Shelf-Stable Fruits and Vegetables

November gains exceeded those in October for fresh fruit, frozen vegetables and canned vegetables. The other areas continued to see the slow month-over-month erosion we have been documenting since July.

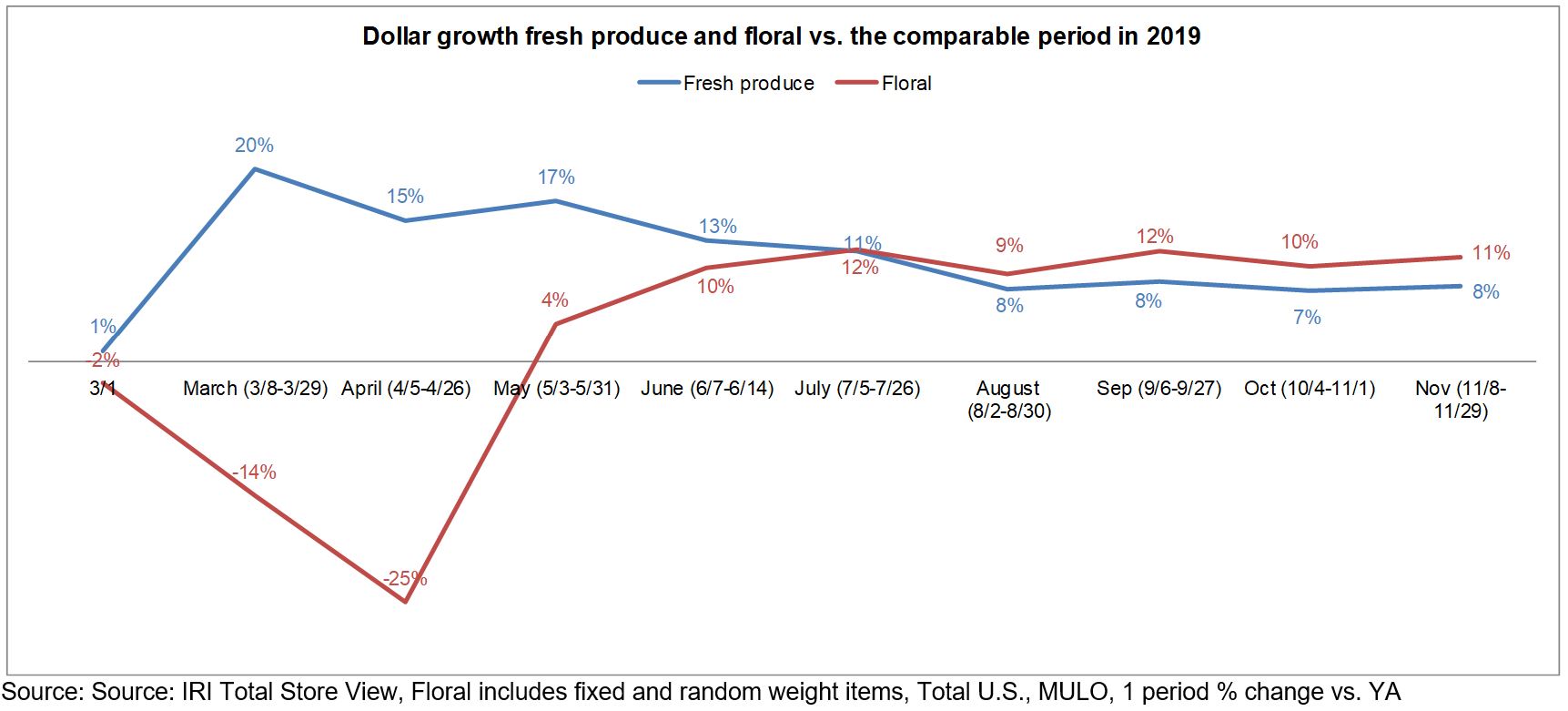

Floral

Floral sales continued to trend in the double-digits above year ago levels, with a gain of 11% in November. This marks six months of gains right around 10% above 2019 levels, which bodes well for the remainder of the year.

Perimeter Performance

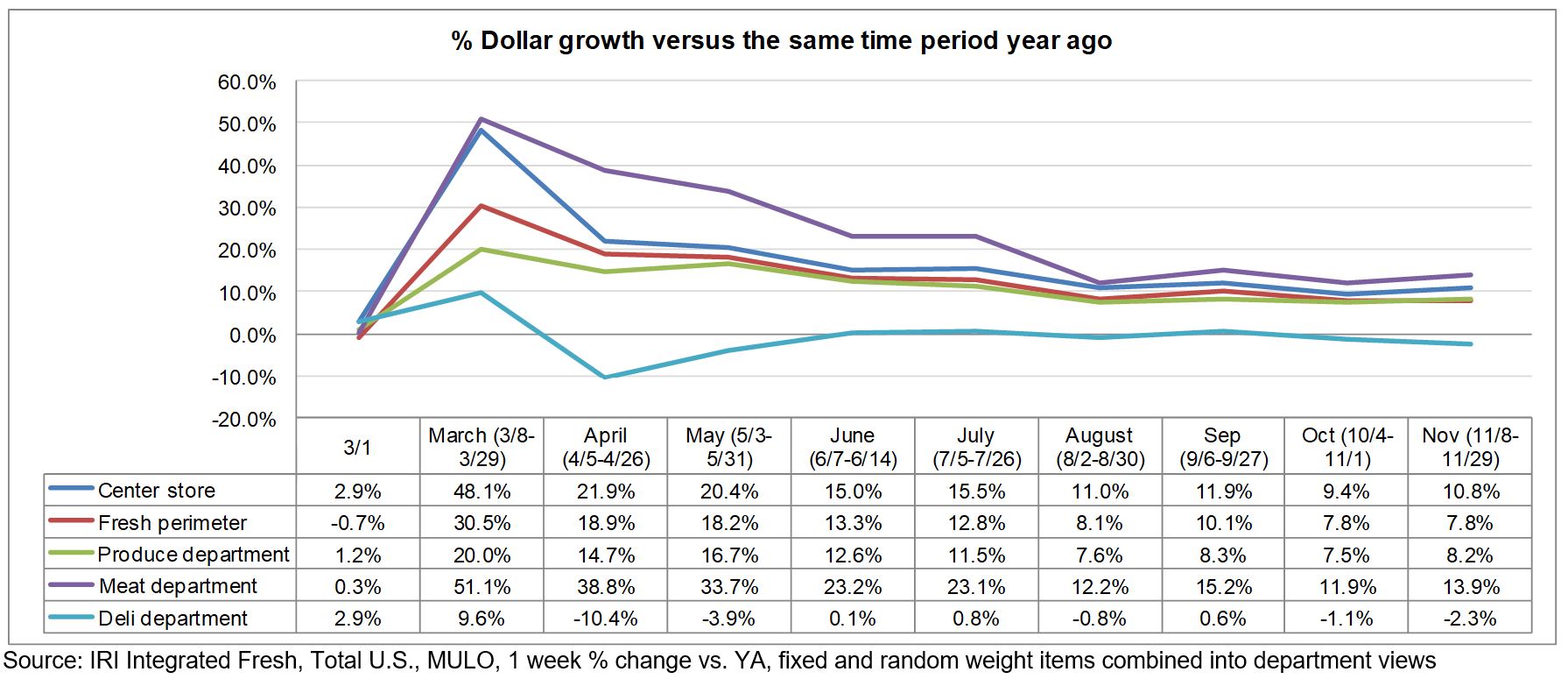

A look across departments shows that the meat department was the only one to exceed total center store grocery. Meat sales were up 13.9% over November. The deli department continued to sit right around year ago levels, sometimes slightly ahead, sometimes slightly behind.

What’s Next?

Everyday demand continues to drive strong vegetable sales and slightly weaker fruit sales — though still well ahead of last year’s levels. Concern over COVID-19 is rising again after falling over the summer and early fall. In the November 13-15 IRI survey wave with primary shoppers, half of Americans were more concerned about COVID-19 than they were the week before. This is almost double the rate as seen in mid-October with rising concern among all age groups. This is driving people back to ecommerce, for groceries and holiday shopping.

Stockpiling rates also started to rise again, with almost a third stocking up on pantry staples/essentials more in the past two weeks than before COVID-19 (up from 24% a month ago). This was not enough to impact availability for most products, however, there was a slight increase in toilet paper out-of-stock issues.

Looking toward the end-of-year holidays, 44% of Americans are worried that the holiday celebrations will cause a spike in COVID cases and over one-third are not looking forward to the holiday season as much as usual because their celebrations will be curtailed. Americans are planning to reduce their gatherings as they did for Thanksgiving. Only one in four plan to celebrate with others outside their household, about half the rate of last year.

- One in three expect to spend less on groceries for the December holidays this year, primarily due to hosting fewer/no guests this year or cutting back to save money.

- Gifting is also expected to be somewhat suppressed. Among those who typically buy gifts, 29% plan to spend less. This will be partially offset by the 14% who plan to spend more on gifts to make the holidays extra special.

- Shoppers plan to spend less on groceries, gifts, and decorations across Grocery, Club, Dollar, local small business, and especially Mass Merch and Drug. Online-only retailers are the only channel where shoppers expect to spend more this year than last year.

- For New Year’s, 30% plan to celebrate at home without guests, while only 5% of primary grocery shoppers plan to go to a party/gathering, 4% host others, and 3% go to a bar/restaurant. 10% celebrated last year but won’t do anything either at home or away from home to ring in the New Year (51% typically don’t celebrate).

“Manufacturers and retailers may consider messaging and promotions that help shoppers find new ways to make the holidays special at home or on a tighter budget, and retailers should plan for an earlier spike in holiday item purchasing than last year,” added Parker.

The next report, covering December, will be released in mid-January. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.

The next report, covering December, will be released in mid-January. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.