According to the U.S. Bureau of Labor Statistics, nearly one in five U.S. businesses fail within the first year.

This number might seem surprisingly low, given any preconceived notion we may have. But for added context, after the first year, new business failure rates increase. After the second year, almost a third fail; by the fifth year, nearly half have failed; and by the tenth year, nearly-two thirds of businesses fail.

The reasons for businesses fail are well established: undercapitalization, stiff competition, no market, poor team performance, or even pricing.

Despite U.S. new business failure statistics, closures—or more specifically, financially stressed business closures—are down over recent years.

According to uscourts.gov, Chapter 7 bankruptcy business filings during the 12 month periods ending June 2022 were 7,635 compared to the 12-month period ending in June 2021, which was 10,466. For the 12-month periods ending June 2020, 2019, and 2018, cases filed were 13,417, 13,788. and 13,679 respectively.

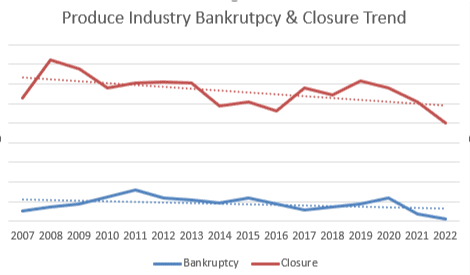

Bankruptcy data and out-of-business statistics from Blue Book Services show a similar declining pattern (see Table 1).

Table 1

In fact, Blue Book closure data is at a 15-year low—so what is unusual about 2022?

Government stimulus programs, lower interest rates, and higher debt forbearance may all be contributing factors during the present, and perhaps since 2020.

With stimulus funding running out, rising interest rates, and high inflation, how will businesses prepare for a snap back to the norm?

Every year, Blueprints discusses a company that closed its doors during the prior year. Our objective is to see if we, as credit extenders, can learn from the company’s decline or help reinforce processes to minimize future negative experiences.

The following case study is intended to provide insight (or hindsight) and lead to more proactive steps when it comes to authorizing a sale to a new prospect or when the next customer begins to fail.

This is an excerpt from the Credit and Finance feature in the January/February 2023 issue of Produce Blueprints Magazine. Click here to read the whole issue.

According to the U.S. Bureau of Labor Statistics, nearly one in five U.S. businesses fail within the first year.

This number might seem surprisingly low, given any preconceived notion we may have. But for added context, after the first year, new business failure rates increase. After the second year, almost a third fail; by the fifth year, nearly half have failed; and by the tenth year, nearly-two thirds of businesses fail.

The reasons for businesses fail are well established: undercapitalization, stiff competition, no market, poor team performance, or even pricing.

Despite U.S. new business failure statistics, closures—or more specifically, financially stressed business closures—are down over recent years.

According to uscourts.gov, Chapter 7 bankruptcy business filings during the 12 month periods ending June 2022 were 7,635 compared to the 12-month period ending in June 2021, which was 10,466. For the 12-month periods ending June 2020, 2019, and 2018, cases filed were 13,417, 13,788. and 13,679 respectively.

Bankruptcy data and out-of-business statistics from Blue Book Services show a similar declining pattern (see Table 1).

Table 1

In fact, Blue Book closure data is at a 15-year low—so what is unusual about 2022?

Government stimulus programs, lower interest rates, and higher debt forbearance may all be contributing factors during the present, and perhaps since 2020.

With stimulus funding running out, rising interest rates, and high inflation, how will businesses prepare for a snap back to the norm?

Every year, Blueprints discusses a company that closed its doors during the prior year. Our objective is to see if we, as credit extenders, can learn from the company’s decline or help reinforce processes to minimize future negative experiences.

The following case study is intended to provide insight (or hindsight) and lead to more proactive steps when it comes to authorizing a sale to a new prospect or when the next customer begins to fail.

This is an excerpt from the Credit and Finance feature in the January/February 2023 issue of Produce Blueprints Magazine. Click here to read the whole issue.

Bill Zentner is Vice President, Ratings Service for Blue Book