“In December, we saw consumers moving around much more than any other month during the pandemic,” said Jonna Parker, Team Lead Fresh for IRI. “But come February, trips and basket size trends moved back to the patterns that we saw throughout most of 2020. Trips fell below 2020 levels in February, whereas the spend per trip remained highly elevated. This means food spending remained home-centric, which benefits produce as part of many breakfast, lunch, dinner, snacking and beverage occasions.”

Sales of all food and beverage related items remained elevated from January’s strong increase of +12.0%. February sales increased 11.8% over the weeks ending February 3rd through February 28th versus the same weeks in 2020. Both months are up significantly from a subdued December (+8.1%).

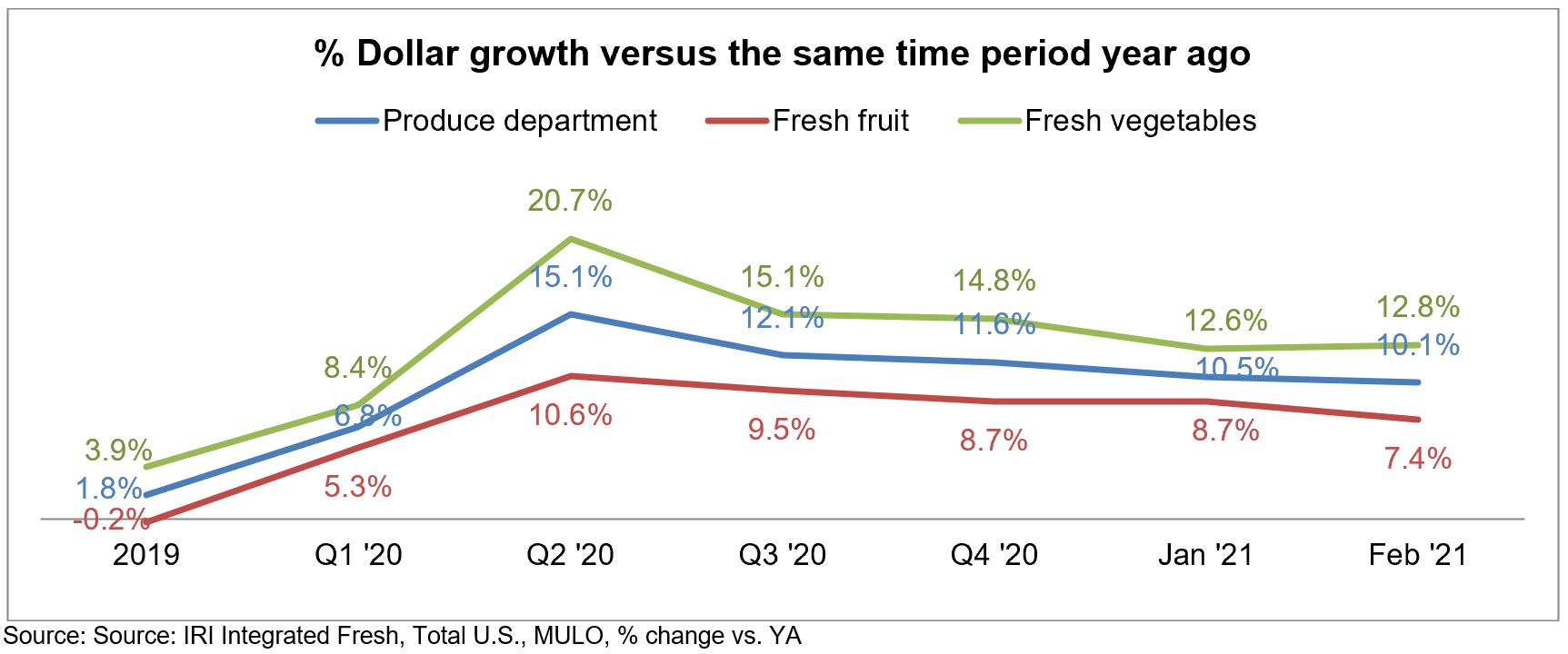

February produce department sales for the five weeks ending 2/28/2021 increased +10.1%, excluding online-only and delivery e-commerce sales that would have been significantly higher than in 2020. Fresh produce added $483 million versus the comparable period in 2020. As seen throughout the pandemic, frozen fruits and vegetables had the highest growth, but are also the smallest sales of the three temperature zones in retail.

“February had two holidays, Super Bowl and Valentine’s Day, where we typically see a significant part of the dollars go to foodservice,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “While restaurants are starting to reopen in many states, retail still saw an above-average boost with many grocers offering meal solutions for Super Bowl entertaining and Valentine’s Day at home. Additionally, everyday demand continues to be elevated as the majority of the nation’s school-aged children remain in virtual or hybrid education and many people are still working from home.”

Fresh produce generated $5.3 billion in sales during the four February weeks. This reflects $169 million in additional fruit sales and $314 million in additional vegetable sales in February 2021 versus a year ago.

Fresh Share

In 2019, fresh produce sales represented 80.8% of total fruits and vegetables sales across the store. That share fell as low as 76.9% during the first quarter of 2020, pulled down by the March panic buying weeks when many dollars were diverted to frozen and canned. The fresh share briefly recovered in the second and third quarters but as the number of new COVID-19 cases spiked once more in November and December, the fresh share once more dropped to 77.7%. February 2021 showed a slight recovery of the fresh dollar share to 79.1% — a percentage point higher than January.

Fresh Produce Dollars versus Volume

Fresh produce dollars have been outpacing volume since the onset of the pandemic — pointing to inflation as well as more premium purchase choices from consumers. In February 2021, the gap between volume and dollar gains widened to 3.0 percentage points, up from 1.6 in the fourth quarter of 2020. “The strength of vegetables remains remarkable whether we look at dollar or volume gains at retail,” said Watson. “But it is also important to acknowledge the total category sales across retail and foodservice may be down based on combined demand. Additionally, the strength of vegetables is not a new trend. Vegetables have been outgrowing fruit for several years now. That said, the gap between volume and dollar growth for fruit is starting to widen significantly after seeing on-and-off deflation throughout 2020.” In January, eating healthier was the top resolution among shoppers according to IRI’s monthly shopper survey. While a perennial favorite New Year’s theme, the rate was stronger in 2021 and purchases point to a big focused on immunity building.

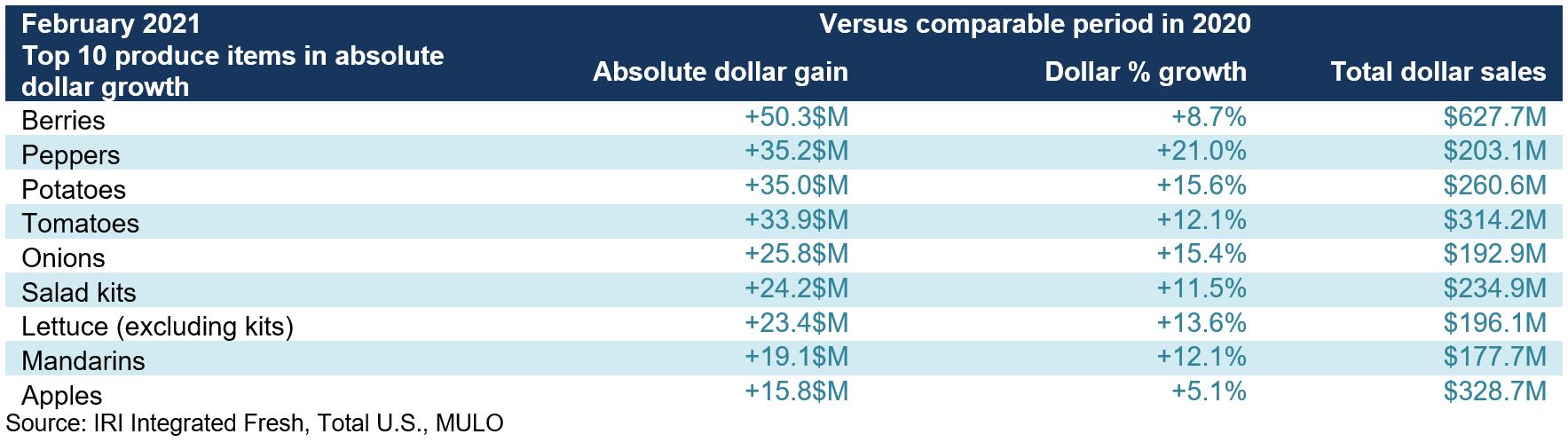

Absolute Dollar Gains

“The February 2021 Top 10 in absolute dollar gains is once more led by berries that generated an additional $50.3 million in sales,” said Watson. “The dominance of vegetables is also clear from looking at the top growers in February that includes seven vegetables and three fruits.”

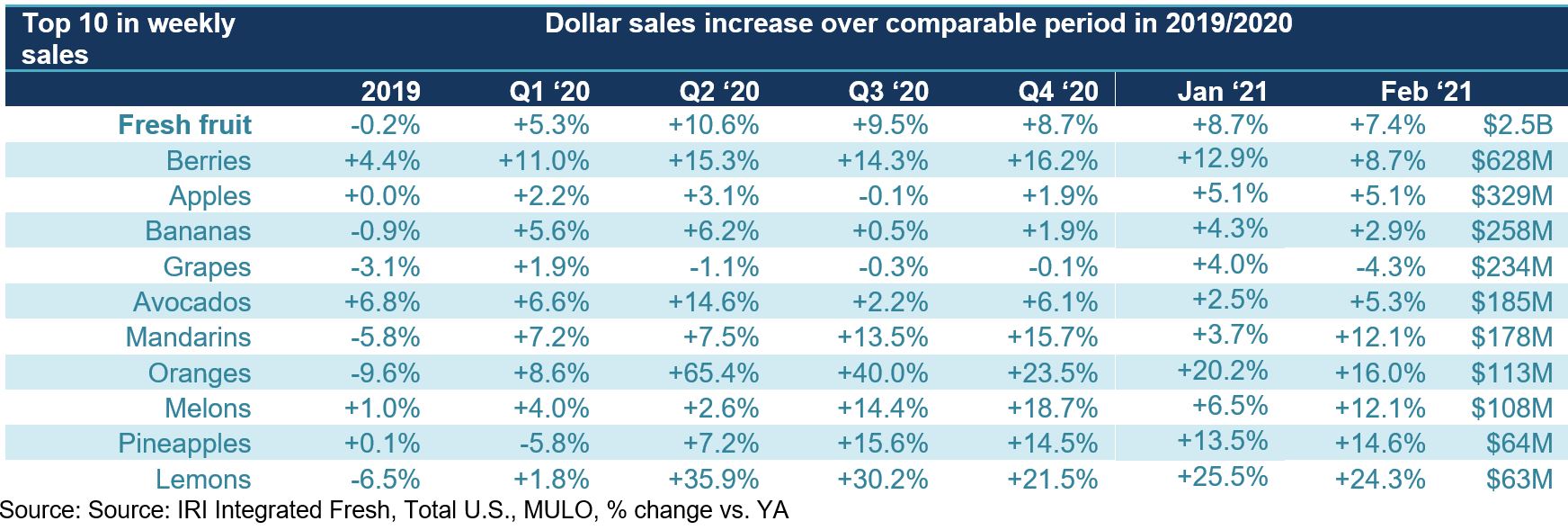

Fresh Fruit

“In fruit, apples are making their size and power known in February,” said Parker. “While berries are still the dominant sales engine they have been for some time, apples generated nearly $330 million — matching their January gain of 5.1%. Avocados also had a strong February, no doubt related to Super Bowl sales.”

Citrus fruit continued to grow at a fast pace, up 16.6% in February. Only grapes lost some ground versus year ago levels while lemons and oranges were the fastest growers.

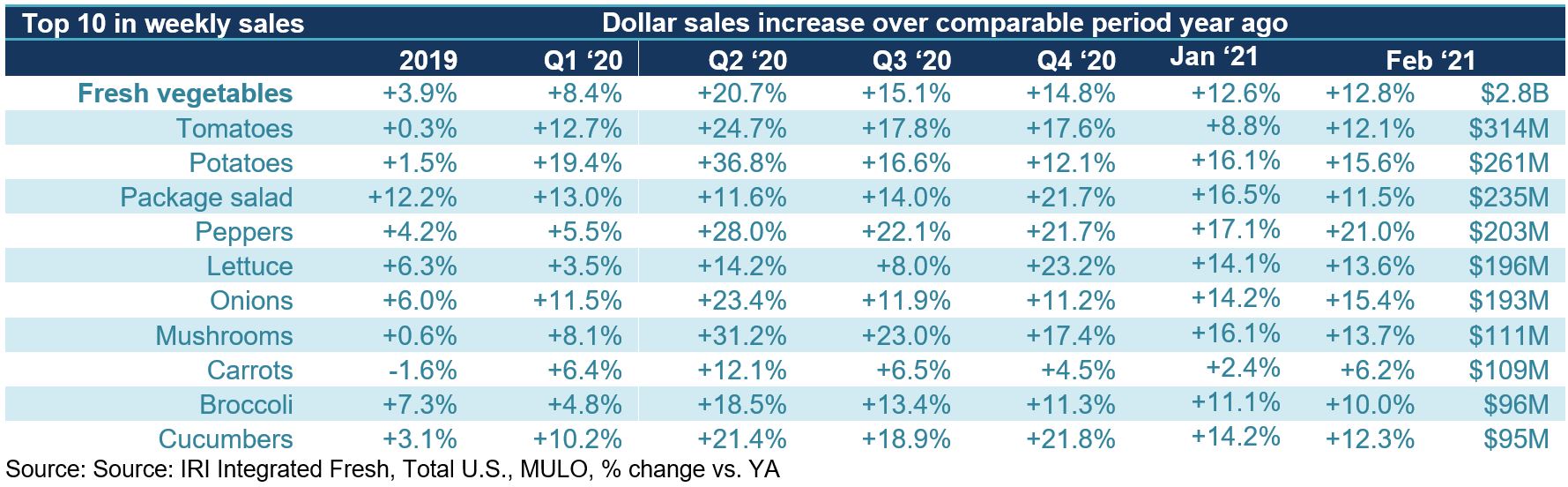

Fresh Vegetables

“The vegetable side reflects double-digit gains for nine out of the 10 items,” said Watson. “This once more underscores why vegetables have been so dominant throughout the pandemic. With consumers bored with the same old meals and growing tired of cooking so many more meals at home at the same time, it is important to continue to provide tips and suggestions to encourage variety and trial. In looking at our neighbors in the perimeter, we see tremendous strength in seafood as well as smaller meats, such as lamb and bison. Providing suggestions on vegetable pairings can be a great way to start whole new routines.”

Fresh versus Frozen and Shelf-Stable Fruits and Vegetables

Frozen fruit and vegetables continued their winning streak in the first month of 2021, with an increase of 15.0% over year ago levels. Canned fruit and vegetables have been in single-digits for several months now, while sales patterns for fresh and frozen are holding fairly steady.

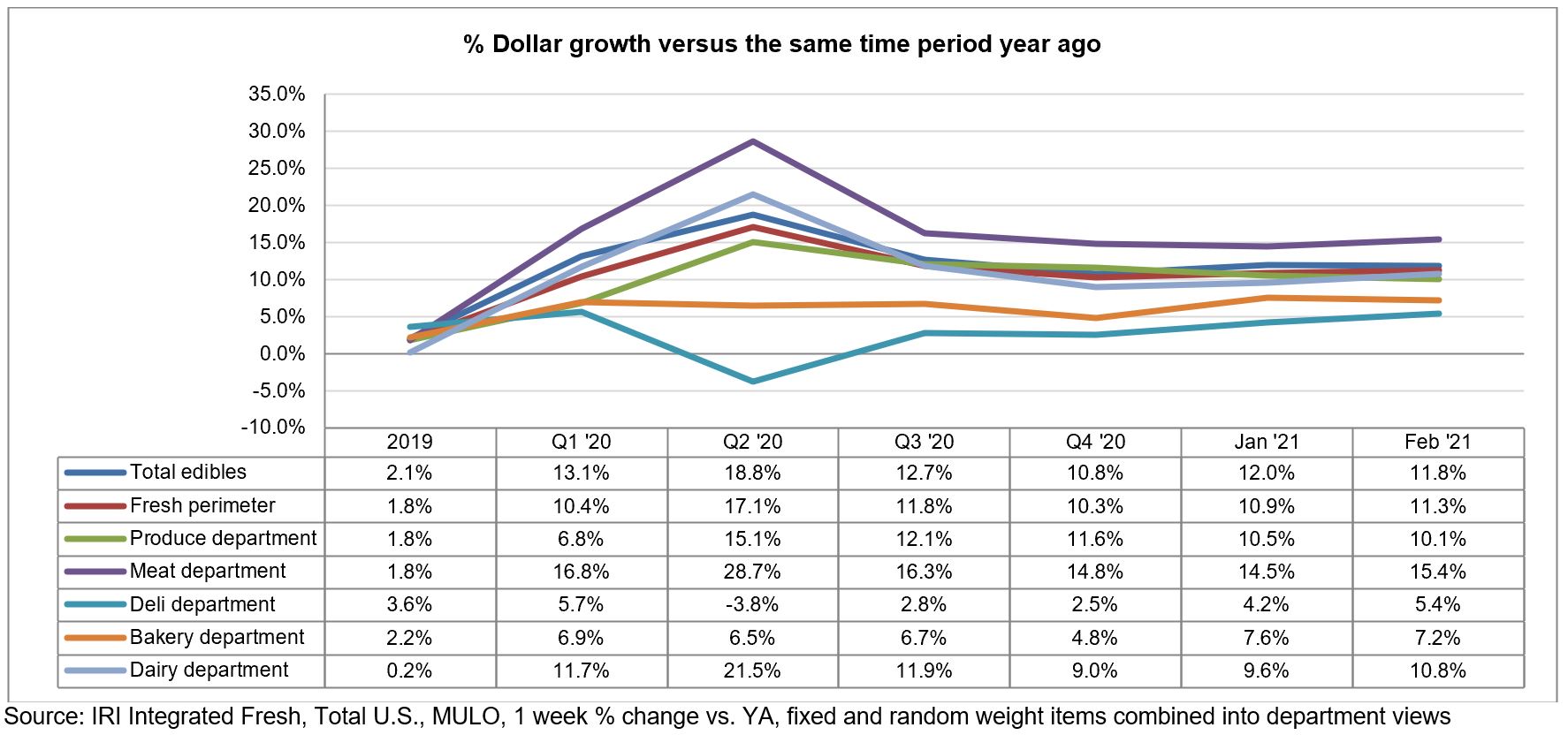

Perimeter Performance

A look across departments for the four weeks ending February 28, 2021 versus year ago shows that center store foods and beverages outpaced the perimeter. Fresh department sales were pulled up by a strong month for meat, with an on-average performance for produce.

What’s Next?

In March 2021, sales will go up against the two biggest weeks in the history of grocery retailing and will likely turn negative versus year ago. However, based on the pattern of the last few months, sales are likely still going to track ahead against the baseline of 2019. Additionally, produce still has an opportunity to find pockets of growth by encouraging engagement across a wider number of items and meal occasions.

With the average number of new COVID-19 cases coming down and vaccinations increasing, pent up demand for eating out is likely going to increase foodservice spending, particularly as more states are opening up on-premise dining. Additionally, increases in gasoline sales, OpenTable reservations, TSA checkpoint numbers, the re-opening of schools and other indicators are pointing to increased consumer mobility. Increased mobility is also likely to result in a switch from home-centric food spending to greater foodservice engagement, and may drive increased demand for time-saving, convenience focused solutions in the produce department.

With an early Easter, on April 4, March is likely going to see a spike in Easter powerhouses. It is unlikely that gatherings will be back to pre-pandemic group sizes as travel remains below typical levels. Deli-prepared holiday meal solutions have seen tremendous success for the summer, fall and winter holidays and are likely to be a win for the upcoming Easter holiday as well.

The next report, covering March, will be released in mid-April. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.

The next report, covering March, will be released in mid-April. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.

Date ranges:

- 2019: 52 weeks ending 12/28/2019

- Q1 2020: 13 weeks ending 3/29/2020

- Q2 2020: 13 weeks ending 6/28/2020

- Q3 2020: 13 weeks ending 9/27/2020

- Q4 2020: 13 weeks ending 12/27/2020

- January: 5 weeks ending 1/31/2021

- February: 4 weeks ending 2/28/2021