Investors, shareholders, and analysts use EBITDA (earnings before interest, taxes, depreciation, and amortization) to provide a snapshot of short-term operational efficiency.

A company can report a net loss and still be considered profitable if its EBITDA value is positive.

As a measure of a company’s ability to generate profit, regardless of its debt structure, EBITDA does not take capital expenditures (“CapEx”) or debt payments into account. For this reason, it is useful for comparing same-industry companies with different capital structures and debt profiles.

Many companies minimize their taxable net income by maximizing the depreciation or amortization expensed in a given year. When comparing a company that minimizes its net income via this method against another company with an opposite strategy, EBITDA allows for an apples-to-apples comparison, as it neutralizes the effects of depreciation and amortization.

As a percentage of total revenue, EBITDA can be used to compare the relative profitability of two same-industry companies.

For example, if company A reports $10 in net profit on $100 of revenue, and company B reports $5 in net profit on $100 of revenue, it may appear on the surface that company A (10 percent profit margin) is converting its revenue to profits more efficiently than company B (5 percent profit margin).

However, if company B expensed $15 of amortization on its income statement for that period, the actual cash created by company B changes to $20 (20 percent EBITDA margin).

Banks use EBITDA as the backbone of their debt service coverage calculations to evaluate business loan requests. Commercial lenders take EBITDA, subtract cash paid for CapEx and distributions paid to the shareholders, and set the resulting cash flow available against the required debt payments. This ‘debt service coverage ratio’ is often used as a loan covenant.

Another popular bank covenant is cash flow leverage, which is calculated by taking the amount of third-party financing on the balance sheet and setting it against EBITDA. This “funded debt to EBITDA” ratio indicates how many years it may take for the company to generate enough cash to pay off its existing financed debt.

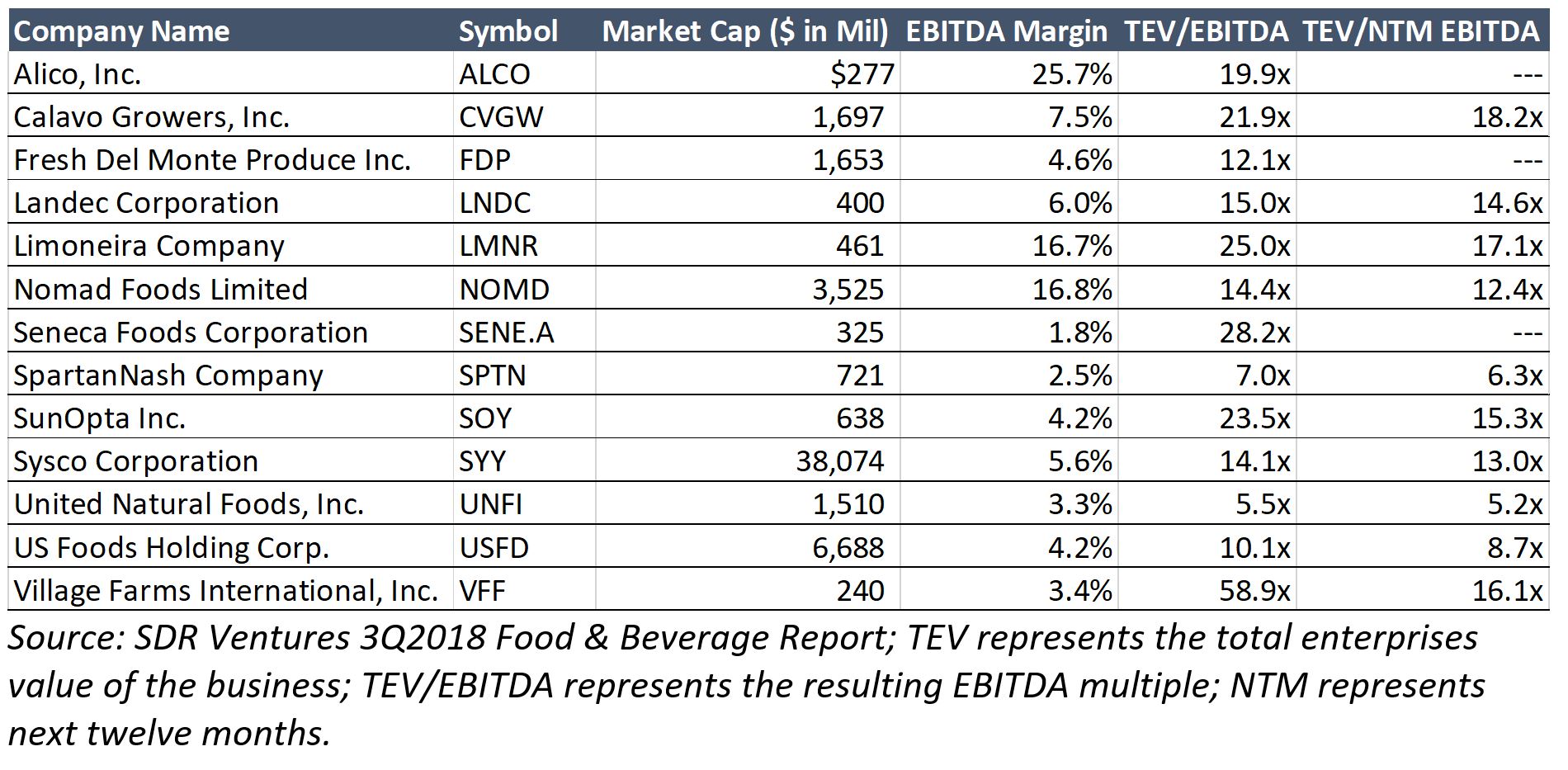

Investors and analysts use multiples of adjusted EBITDA to determine the value of a business. David Sneddon, assistant vice president of sponsor finance at BMO Harris Bank, states that essentially “every middle market company being sold will be valued on a multiple of EBITDA.”

The multiples used vary across industries and by point in the larger economic cycle (expansion or recession). As illustrated by the graph, when investors or bankers believe in the stability of the economy, they are willing to pay or lend higher multiples of EBITDA to acquire a company. This is because they’re more confident in the sustainability of the company’s earning power to service a higher debt load or acquisition cost.

This is an excerpt from the most recent Produce Blueprints quarterly journal. Click here to read the full version.

Investors, shareholders, and analysts use EBITDA (earnings before interest, taxes, depreciation, and amortization) to provide a snapshot of short-term operational efficiency.

A company can report a net loss and still be considered profitable if its EBITDA value is positive.

As a measure of a company’s ability to generate profit, regardless of its debt structure, EBITDA does not take capital expenditures (“CapEx”) or debt payments into account. For this reason, it is useful for comparing same-industry companies with different capital structures and debt profiles.

Many companies minimize their taxable net income by maximizing the depreciation or amortization expensed in a given year. When comparing a company that minimizes its net income via this method against another company with an opposite strategy, EBITDA allows for an apples-to-apples comparison, as it neutralizes the effects of depreciation and amortization.

As a percentage of total revenue, EBITDA can be used to compare the relative profitability of two same-industry companies.

For example, if company A reports $10 in net profit on $100 of revenue, and company B reports $5 in net profit on $100 of revenue, it may appear on the surface that company A (10 percent profit margin) is converting its revenue to profits more efficiently than company B (5 percent profit margin).

However, if company B expensed $15 of amortization on its income statement for that period, the actual cash created by company B changes to $20 (20 percent EBITDA margin).

Banks use EBITDA as the backbone of their debt service coverage calculations to evaluate business loan requests. Commercial lenders take EBITDA, subtract cash paid for CapEx and distributions paid to the shareholders, and set the resulting cash flow available against the required debt payments. This ‘debt service coverage ratio’ is often used as a loan covenant.

Another popular bank covenant is cash flow leverage, which is calculated by taking the amount of third-party financing on the balance sheet and setting it against EBITDA. This “funded debt to EBITDA” ratio indicates how many years it may take for the company to generate enough cash to pay off its existing financed debt.

Investors and analysts use multiples of adjusted EBITDA to determine the value of a business. David Sneddon, assistant vice president of sponsor finance at BMO Harris Bank, states that essentially “every middle market company being sold will be valued on a multiple of EBITDA.”

The multiples used vary across industries and by point in the larger economic cycle (expansion or recession). As illustrated by the graph, when investors or bankers believe in the stability of the economy, they are willing to pay or lend higher multiples of EBITDA to acquire a company. This is because they’re more confident in the sustainability of the company’s earning power to service a higher debt load or acquisition cost.

This is an excerpt from the most recent Produce Blueprints quarterly journal. Click here to read the full version.

Abigail Taylor is an assistant vice president of commercial lending at Wheaton Bank & Trust Company in Wheaton, IL (a Wintrust Community Bank) and has been with the company since 2012. She earned a business economics degree from Wheaton College in Illinois.