Rabobank has published its latest World Vegetable Map, charting recent global vegetable production, consumption, and trade.

The value of the vegetable trade rose in line with rising prices, reaching 3% average annual growth from 2017 to 2022. Production in the EU and the US saw declines over the same period. Consumption has held up relatively well despite higher costs for consumers and producers alike.

“The past five years have been everything but boring for the vegetable sector,” says Cindy van Rijswick, Global Strategist – Fresh Produce at Rabobank. “The Covid-19 pandemic, extreme weather events, skyrocketing costs for growers, and challenging logistics are just some of the factors that have impacted the sector.”

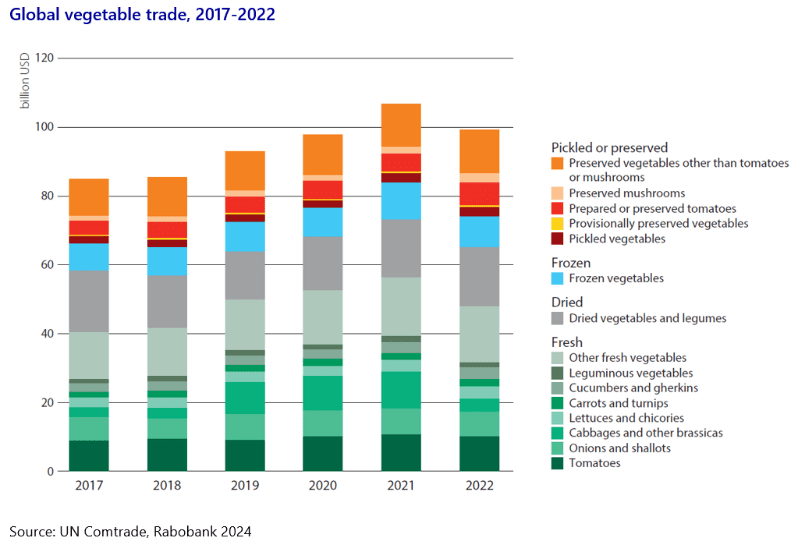

Despite these challenges, global trade in both processed and fresh vegetables increased by an average of 3% per year from 2017 to 2022, though not in a linear pattern due to the Covid pandemic and subsequent inflation. At its height, global trade was valued at USD 107 billion in 2021, passing the USD 100 billion mark for the first and only time. Compared to trade, global vegetable production grew at a slower pace of 1.2% per year over the same period. Notably, the EU and the US both experienced declines in production.

US largest import market for fresh vegetables; new players in fresh and processed trade

An estimated 7% of vegetables produced globally are traded, mainly within continents and often between neighboring countries.

Van Rijswick: “Since 2017, the US has further cemented its position as the world’s largest import market for fresh vegetables, with a significant share of imports for greenhouse vegetables like cucumbers, tomatoes, and bell peppers. This has led to a nearly 40% increase in Mexico’s total fresh vegetable exports between 2017 and 2022.”

“Mexico, Spain, and the Netherlands have remained relevant exporters in the world of fresh vegetables, and countries such as Turkey and Poland are becoming bigger producers and exporters of both fresh and processed vegetables,” adds Van Rijswick. Poland, in particular, has evolved as both an importer and exporter, reflecting its growing significance as a central European trading hub. Meanwhile, in the processed vegetable market, China now exports more frozen vegetables than Belgium, the previous top exporter.

The clearest trend: Higher costs all around

“The most notable trend in recent years has been cost increases, resulting in higher trade value as well as increased prices in the supermarket,” notes Van Rijswick. Global trade value of frozen vegetables went up in 2021 because of high demand during the pandemic and inflation.

In 2021 and 2022, the cost of making and shipping processed vegetables also increased due to higher prices for vegetables, packaging, logistics, and energy. Inflation affected the fresh vegetable sector too, though to a lesser extent.

“In many cases, prices also increased for consumers,” says Van Rijswick. “Despite inflation, consumption has held up relatively well overall. Still, it is difficult to determine whether inflated vegetable prices have impacted consumer purchasing behavior, as developments vary around the world.”

In Australia, for example, per capita vegetable consumption decreased between 2017 and 2022, despite relatively limited inflation, as consumers shifted to purchasing fewer, but higher-value vegetables. In the US, the overall volume of vegetables consumed did not change much over the same period. German households, in contrast, bought more fresh vegetables, with post-pandemic purchases remaining considerably higher than in 2019, despite the relatively high increase in vegetable prices.

Contact

Melanie Bernds

Public Relations, Rabobank

(636) 331-3589

Melanie.bernds.smith@rabobank.com