September sales slipped 3% while the third quarter finished up 4% versus last year.

September sales slipped 3% while the third quarter finished up 4% versus last year

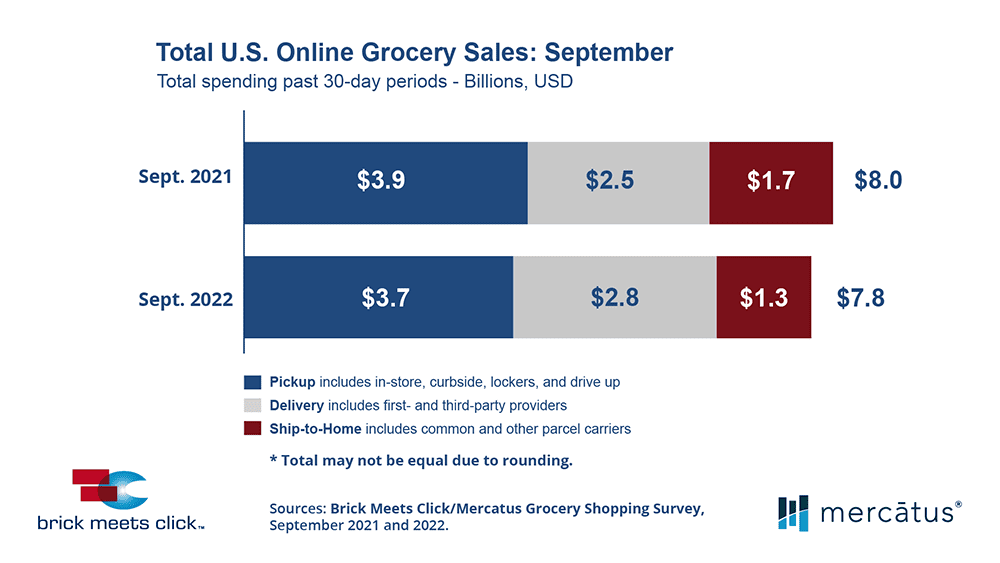

Barrington, IL – October 11, 2022 – Total U.S. online grocery sales in September declined 3% year over year to $7.8 billion according to the monthly Brick Meets Click/Mercatus Grocery Shopping Survey fielded September 29-30, 2022. However, the ongoing research initiative reported that third quarter online grocery sales for 2022 gained nearly 4% to $24.1 billion compared to 2021, driven by significant gains in Delivery and to a lesser degree Pickup.

“These quarterly results reflect the fact that there are now an increasing number of ways to receive eGrocery orders via Delivery,” said David Bishop, Partner at Brick Meets Click. “Today, customers who want to shop their local grocery store typically have the choice of several different Delivery providers and platforms but that is not necessarily the case for Pickup. In addition, national grocers are investing in growing more integrated first-party services that could offer a more acceptable alternative for customers attracted to Delivery.”

Pickup, the largest segment of eGrocery sales, had a mixed third quarter with total sales up 1% despite a 6% drop in September sales versus the prior year. The growth in quarterly sales was the result of shifts in its user base and order frequency being offset by ongoing growth in spending each month.

Specifically, Pickup’s monthly active users (MAUs) fluctuated between July, August, and September, resulting in a 2% contraction of its MAU base for the third quarter compared to last year. Order frequency followed a similar trend, as the number of orders received by active Pickup users expanded in July but shrank in August and September, dipping just over 1% for the quarter. Average order value (AOV) increased each month and finished up 4% for the quarter versus 2021. Pickup ended the third quarter with a 44% share of sales, down 1.2 percentage points versus a year ago.

Delivery had a strong third quarter and continued to benefit from a range of new service options from national players and new third-party providers that helped fuel a 20% lift in sales for the quarter versus the prior year. Each month’s total sales growth, however, slowed sequentially through the quarter with September finishing 12% up from a year ago.

During the quarter, Delivery’s MAU base expanded faster each month compared to the same periods last year, driving growth of more than 6% for the quarter versus 2021. Order frequency remained essentially unchanged on a quarterly basis versus a year ago although it declined during both August and September compared to 2021. Delivery’s AOV for the quarter climbed 12% versus the prior year, causing it to surpass Pickup’s spending by about $5 per order for the same period. As a result, Delivery gained 5.4 points of share in the third quarter versus last year, bringing its share of eGrocery sales for the quarter to almost 39%.

Ship-to-Home experienced another tough quarter as its sales declined by 17% versus 2021. This was only slightly better than its September performance, which was down 19% versus the prior year.

The MAU base for Ship-to-Home contracted at a faster rate each month during the quarter, shrinking nearly 11% in September and ending the third quarter down more than 6% compared to 2021. Order frequency among its MAUs also slowed at a faster rate each consecutive month with September down 11%, and the quarter was off almost 7% compared to the prior year. While Ship-to-Home’s AOV for September grew by 2% versus a year ago, spending per order was down for the quarter nearly 5%. Ship-to-Home ended the third quarter with a 17% share of eGrocery sales, down 4.3 points versus 2021.

The rate of cross-shopping between Grocery and Mass increased during both the most recent month and quarter by more than 2 and 3 percentage points respectively versus prior periods in 2021. For September, the share of households that used both a Grocery and Mass service during the month was 28% while for the quarter the share finished at 29%.

The degree of cross-shopping is a key metric for grocers to monitor because while the overall repeat intent rate has climbed, so has the performance gap between Mass and Grocery. The likelihood that an online grocery customer will use the same service again within the next 30 days gained 3 percentage points to 63% for the quarter. More importantly, the specific repeat intent rate among Mass customers for September 2022 was 10 percentage points higher compared to Grocery customers, and this gap has grown by nearly 7 points since a year ago.

“Successful online grocery retailers are able to navigate competing business priorities, manage through resource constraints, and keep a tight focus on building customer demand,” said Sylvain Perrier, president and CEO, Mercatus. “Getting an online customer to shop again is directly linked to the shopping experience, from the moment they start to build a basket to the moment they receive it. Retailers who can consistently deliver against the promise and expectations associated with online grocery shopping are being rewarded by customers with repeat business.”

Check out the eGrocery Dashboard for September 2002 or visit the eMarket/eShopper page for additional insights and information.

About this consumer research

The Brick Meets Click/Mercatus Grocery Shopping Survey is an ongoing independent research initiative created and conducted by Brick Meets Click and sponsored by Mercatus. Brick Meets Click conducted the survey on September 29-30, 2022, with 1,752 adults, 18 years and older, who participated in the household’s grocery shopping.

The three receiving methods for online grocery orders are defined as follows:

- Delivery includes orders received from a first- or third-party provider like Instacart, Shipt or the retailer’s own employees.

- Pickup includes orders that are received by customers either inside or outside a store or at a designated location/locker.

- Ship-to-Home includes orders that are received via common or contract carriers like FedEx, UPS, USPS, etc.

Results were adjusted based on internet usage among U.S. adults to account for the non-response bias associated with online surveys. Responses are geographically representative of the U.S. and weighted by age to reflect the national population of adults, 18 years and older, according to the U.S. Census Bureau. Brick Meets Click used a similar methodology for each of the surveys conducted in 2022 – Aug. 29-30 (n=1,743), July 29-30 (n=1,690), June 29-30 (n=1,743), May 28-29 (n=1,802), Apr. 28-29 (n=1,746), Mar. 28-29 (n=1,681), Feb. 26-27 (n=1,790), and Jan. 29-30 (n=1,793); in 2021 – Dec. 29-30 (n = 1,836), Nov. 29-30 (n=1,785), Oct. 29-30 (n=1,751), Sept. 28-29 (n=1,728), Aug. 29-30 (n=1,806), July 29-30 (n=1,892), June 27-28 (n=1,789), May 28-30 (n=1,872), Apr. 26-28 (n=1,941), Mar. 26-28 (n=1,811), Feb. 26-28 (n= 1,812), and Jan. 28-31 (n=1,776); in 2020 – Nov. 11-14 (n=2,067), Aug. 24-26 (n=1,817), Jun. 24-25 (n=1,781), May 20-22 (n=1,724), Apr. 22-24 (n= 1,651), and Mar. 23-25 (n=1,601); and in 2019 – Aug. 22-24 (n = 2,485).

About Brick Meets Click

Brick Meets Click is an analytics and strategic insight firm that connects today’s grocery business with tomorrow’s needs. Our clear thinking and practical solutions help clients make their strategies and customer offers more compelling and relevant in the changing U.S. grocery market. We bring deep industry expertise and fact-based analysis to the challenge of finding new routes to success.

About Mercatus

Mercatus helps leading grocers get back in charge of their eCommerce experience, empowering them to deliver exceptional retailer-branded, end-to-end online shopping, from store to door. Our expansive network of more than 50 integration partners allows grocers to work with their partners of choice, on their terms. Together, we enable clients to create authentic digital shopping experiences with solutions to drive shopper engagement, grow share of wallet and achieve profitability, while quickly adapting to changes in consumer behavior. The Mercatus Digital Commerce platform is used by leading North American retailers, including Weis Markets, Save Mart brands, Brookshire’s Grocery Company, Kowalski’s Markets, WinCo Foods, Smart & Final, Stater Bros. Markets and others.

September sales slipped 3% while the third quarter finished up 4% versus last year

Barrington, IL – October 11, 2022 – Total U.S. online grocery sales in September declined 3% year over year to $7.8 billion according to the monthly Brick Meets Click/Mercatus Grocery Shopping Survey fielded September 29-30, 2022. However, the ongoing research initiative reported that third quarter online grocery sales for 2022 gained nearly 4% to $24.1 billion compared to 2021, driven by significant gains in Delivery and to a lesser degree Pickup.

“These quarterly results reflect the fact that there are now an increasing number of ways to receive eGrocery orders via Delivery,” said David Bishop, Partner at Brick Meets Click. “Today, customers who want to shop their local grocery store typically have the choice of several different Delivery providers and platforms but that is not necessarily the case for Pickup. In addition, national grocers are investing in growing more integrated first-party services that could offer a more acceptable alternative for customers attracted to Delivery.”

Pickup, the largest segment of eGrocery sales, had a mixed third quarter with total sales up 1% despite a 6% drop in September sales versus the prior year. The growth in quarterly sales was the result of shifts in its user base and order frequency being offset by ongoing growth in spending each month.

Specifically, Pickup’s monthly active users (MAUs) fluctuated between July, August, and September, resulting in a 2% contraction of its MAU base for the third quarter compared to last year. Order frequency followed a similar trend, as the number of orders received by active Pickup users expanded in July but shrank in August and September, dipping just over 1% for the quarter. Average order value (AOV) increased each month and finished up 4% for the quarter versus 2021. Pickup ended the third quarter with a 44% share of sales, down 1.2 percentage points versus a year ago.

Delivery had a strong third quarter and continued to benefit from a range of new service options from national players and new third-party providers that helped fuel a 20% lift in sales for the quarter versus the prior year. Each month’s total sales growth, however, slowed sequentially through the quarter with September finishing 12% up from a year ago.

During the quarter, Delivery’s MAU base expanded faster each month compared to the same periods last year, driving growth of more than 6% for the quarter versus 2021. Order frequency remained essentially unchanged on a quarterly basis versus a year ago although it declined during both August and September compared to 2021. Delivery’s AOV for the quarter climbed 12% versus the prior year, causing it to surpass Pickup’s spending by about $5 per order for the same period. As a result, Delivery gained 5.4 points of share in the third quarter versus last year, bringing its share of eGrocery sales for the quarter to almost 39%.

Ship-to-Home experienced another tough quarter as its sales declined by 17% versus 2021. This was only slightly better than its September performance, which was down 19% versus the prior year.

The MAU base for Ship-to-Home contracted at a faster rate each month during the quarter, shrinking nearly 11% in September and ending the third quarter down more than 6% compared to 2021. Order frequency among its MAUs also slowed at a faster rate each consecutive month with September down 11%, and the quarter was off almost 7% compared to the prior year. While Ship-to-Home’s AOV for September grew by 2% versus a year ago, spending per order was down for the quarter nearly 5%. Ship-to-Home ended the third quarter with a 17% share of eGrocery sales, down 4.3 points versus 2021.

The rate of cross-shopping between Grocery and Mass increased during both the most recent month and quarter by more than 2 and 3 percentage points respectively versus prior periods in 2021. For September, the share of households that used both a Grocery and Mass service during the month was 28% while for the quarter the share finished at 29%.

The degree of cross-shopping is a key metric for grocers to monitor because while the overall repeat intent rate has climbed, so has the performance gap between Mass and Grocery. The likelihood that an online grocery customer will use the same service again within the next 30 days gained 3 percentage points to 63% for the quarter. More importantly, the specific repeat intent rate among Mass customers for September 2022 was 10 percentage points higher compared to Grocery customers, and this gap has grown by nearly 7 points since a year ago.

“Successful online grocery retailers are able to navigate competing business priorities, manage through resource constraints, and keep a tight focus on building customer demand,” said Sylvain Perrier, president and CEO, Mercatus. “Getting an online customer to shop again is directly linked to the shopping experience, from the moment they start to build a basket to the moment they receive it. Retailers who can consistently deliver against the promise and expectations associated with online grocery shopping are being rewarded by customers with repeat business.”

Check out the eGrocery Dashboard for September 2002 or visit the eMarket/eShopper page for additional insights and information.

About this consumer research

The Brick Meets Click/Mercatus Grocery Shopping Survey is an ongoing independent research initiative created and conducted by Brick Meets Click and sponsored by Mercatus. Brick Meets Click conducted the survey on September 29-30, 2022, with 1,752 adults, 18 years and older, who participated in the household’s grocery shopping.

The three receiving methods for online grocery orders are defined as follows:

- Delivery includes orders received from a first- or third-party provider like Instacart, Shipt or the retailer’s own employees.

- Pickup includes orders that are received by customers either inside or outside a store or at a designated location/locker.

- Ship-to-Home includes orders that are received via common or contract carriers like FedEx, UPS, USPS, etc.

Results were adjusted based on internet usage among U.S. adults to account for the non-response bias associated with online surveys. Responses are geographically representative of the U.S. and weighted by age to reflect the national population of adults, 18 years and older, according to the U.S. Census Bureau. Brick Meets Click used a similar methodology for each of the surveys conducted in 2022 – Aug. 29-30 (n=1,743), July 29-30 (n=1,690), June 29-30 (n=1,743), May 28-29 (n=1,802), Apr. 28-29 (n=1,746), Mar. 28-29 (n=1,681), Feb. 26-27 (n=1,790), and Jan. 29-30 (n=1,793); in 2021 – Dec. 29-30 (n = 1,836), Nov. 29-30 (n=1,785), Oct. 29-30 (n=1,751), Sept. 28-29 (n=1,728), Aug. 29-30 (n=1,806), July 29-30 (n=1,892), June 27-28 (n=1,789), May 28-30 (n=1,872), Apr. 26-28 (n=1,941), Mar. 26-28 (n=1,811), Feb. 26-28 (n= 1,812), and Jan. 28-31 (n=1,776); in 2020 – Nov. 11-14 (n=2,067), Aug. 24-26 (n=1,817), Jun. 24-25 (n=1,781), May 20-22 (n=1,724), Apr. 22-24 (n= 1,651), and Mar. 23-25 (n=1,601); and in 2019 – Aug. 22-24 (n = 2,485).

About Brick Meets Click

Brick Meets Click is an analytics and strategic insight firm that connects today’s grocery business with tomorrow’s needs. Our clear thinking and practical solutions help clients make their strategies and customer offers more compelling and relevant in the changing U.S. grocery market. We bring deep industry expertise and fact-based analysis to the challenge of finding new routes to success.

About Mercatus

Mercatus helps leading grocers get back in charge of their eCommerce experience, empowering them to deliver exceptional retailer-branded, end-to-end online shopping, from store to door. Our expansive network of more than 50 integration partners allows grocers to work with their partners of choice, on their terms. Together, we enable clients to create authentic digital shopping experiences with solutions to drive shopper engagement, grow share of wallet and achieve profitability, while quickly adapting to changes in consumer behavior. The Mercatus Digital Commerce platform is used by leading North American retailers, including Weis Markets, Save Mart brands, Brookshire’s Grocery Company, Kowalski’s Markets, WinCo Foods, Smart & Final, Stater Bros. Markets and others.