The fourth quarter of 2021 was disrupted by high levels of COVID-19 cases, high inflation and continued supply chain disruption.

“Americans are very aware of inflation, with 43% perceiving prices to be a little higher and 48% perceiving them to be much higher,” said Jonna Parker, Team Lead for IRI Fresh, citing the December wave of IRI’s primary shopper survey. “Among those who have noticed inflation, 94% are concerned about it. Further, produce is the second most frequently mentioned example by consumers of products with elevated prices. In response to inflationary pressure around the store, 45% look for sales specials more often, 21% buy more private brand and 13% visit different stores. About one-third of shoppers have not (yet) made any changes due to price increases.”

The combined effect of inflation, out-of-stocks and the latest COVID-19 wave resulted in continued changes as it related to choices in food purchasing and consumption. In 2022, IRI, 210 Analytics and the International Fresh Produce Association (IFPA) will continue to team up to document the ever-changing marketplace and its impact on fresh produce sales.

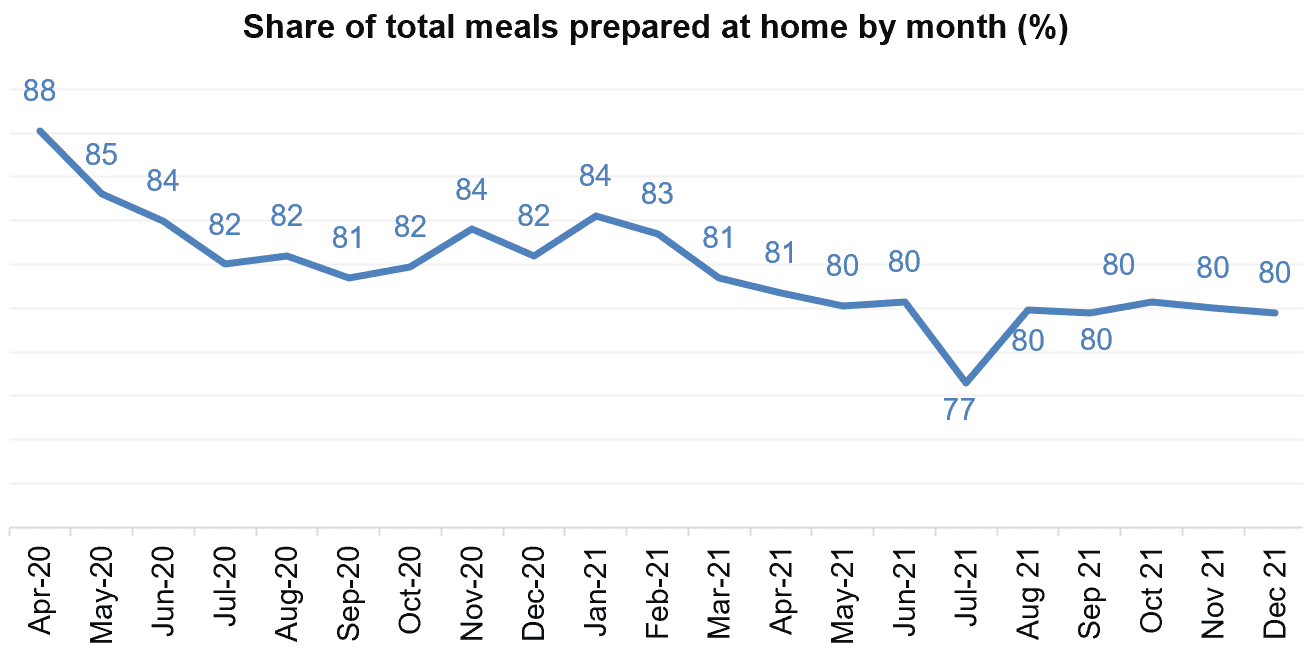

Meals remained home-centric in December. According to the IRI primary shopper survey, the share of meals prepared at home remained at 80%. The share of in-store versus online trips to buy groceries gained a little in December (86%) versus its November levels (83%) — perhaps related to holiday shopping.

During the early months of the pandemic, as many as 20% of trips were online. This dropped to a low of 11% in July of 2021.

Yet online shopping remains a complementary trip for most consumers. In December 2021, only 3% of survey respondents believe they will buy all their groceries online in the next month. This compares to 69% who believe they will buy everything in store, leaving 28% who will mix online and in-store grocery shopping. This signals a likely continuation of mixed format shopping for 2022 for a significant number of people. “Mixed format shopping is an important area to address for fresh produce,” added Parker. “Frozen and canned goods have very high online conversion but not everyone likes buying fresh produce online. Easing online buying hesitations will help build the online fresh produce basket as an important area of growth in 2022.”

Inflation

The consumer price index increased 6.8% for the 12 months ending November 2021, its highest since June 1982, according to the Bureau of Labor Statistics. IRI-measured price per unit for all food and beverages in multi-outlet stores, including supermarkets, club, mass, super-center, drug, military, and other retail food stores, also shows that prices continued to rise over and above their elevated 2020 levels. In December 2021, the average price per unit was up 8.3% versus December 2020 across all food and beverages. For the total year, prices increased 5.3% — pulled down by much milder inflation in the second quarter.

Source: IRI, Integrated Fresh Total US, MULO, inflation index vs. YAGO

Fresh produce prices are also higher than last year. In 2021, price per volume (pound) for total fresh produce increased by 6.5% — pulled down by much milder inflation early on in the year. When regarding inflation in December 2021 only, a comparison to 2020 shows a 14.7% increase for fresh fruit. December inflationary levels are much lower for vegetables, but still average +4.6%.

“Prices across the store and produce specifically are not only a concern for consumers,” said Joe Watson, VP, Retail, Foodservice & Wholesale for IFPA. “Inflation like this affects volume sales and we are a volume-driven business. Consumer efforts to save money typically start with buying what is on sale, but that is another area where we are struggling. Subsequent measures range from simply buying less to buying more frozen or canned, which all pressure volume.”

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. year ago.

2021 Sales

2021 brought $691 billion in food and beverage sales — up 1.8% over 2020 and 15.8% over the 2019 pre-pandemic normal. However, inflation played a significant role with year-on-year unit sales still down 3.3%. Perishables, including produce, seafood, meat, bakery and deli, had the highest year-over-year sales growth in 2021, at +2.2%. Frozen foods had the highest increase versus the pre-pandemic normal of 2019, at +23.0%. The performance by the produce department is right in line with the rest of the store. Year-on-year dollar gains were slightly above average, where the comparison to 2019 tracked slightly behind.

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. year ago.

From a dollar sales perspective, 2021 was another great year for fresh produce, surpassing the records set in 2020. However, dollar gains were inflation boosted and units and volume sales declined year-on-year. “Traditionally we have always compared our performance to the prior year and that is a hard habit to break,” said Watson. “But when we remove the unprecedented demand of 2020 and compare to the more typical levels of 2019, we see our true accomplishment. The fresh produce supply chain moved nearly 43 billion pounds through the registers in 2021, which was 7.1% more than 2019.”

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. year ago.

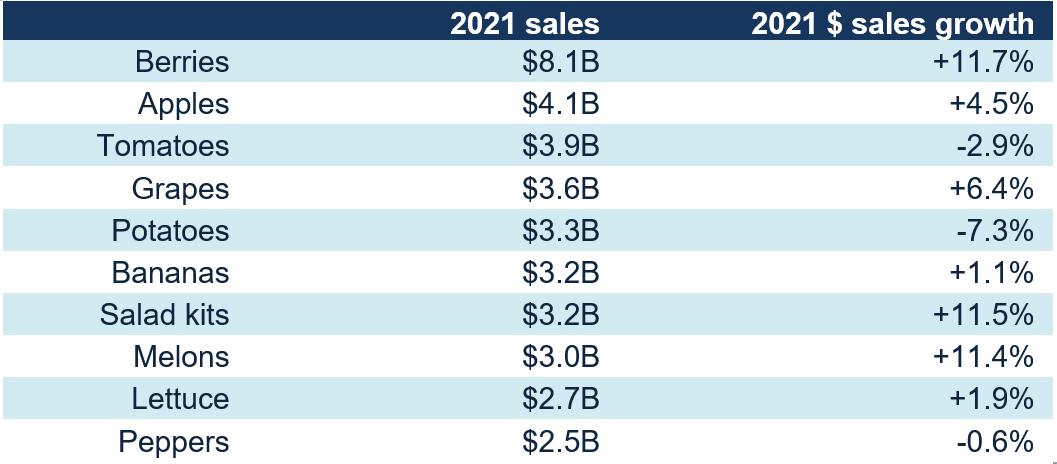

2021 Top Sellers Fruit and Vegetables

Source: IRI Integrated Fresh, Total U.S., MULO

The top sellers in 2021 reflect a mix of fruits and vegetables. Berry sales were nearly twice that of the number two, apples and tomatoes were the biggest seller on the vegetable side. Additionally, berries recorded the highest growth rates among the top 10 sellers, at +11.7%. Other areas with high year-on-year growth were salad kits and melons.

Not all top 10 sellers grew sales in 2021. Tomatoes, potatoes and peppers lost a little ground compared with their 2020 records.

The fourth quarter of 2021 was disrupted by high levels of COVID-19 cases, high inflation and continued supply chain disruption.

“Americans are very aware of inflation, with 43% perceiving prices to be a little higher and 48% perceiving them to be much higher,” said Jonna Parker, Team Lead for IRI Fresh, citing the December wave of IRI’s primary shopper survey. “Among those who have noticed inflation, 94% are concerned about it. Further, produce is the second most frequently mentioned example by consumers of products with elevated prices. In response to inflationary pressure around the store, 45% look for sales specials more often, 21% buy more private brand and 13% visit different stores. About one-third of shoppers have not (yet) made any changes due to price increases.”

The combined effect of inflation, out-of-stocks and the latest COVID-19 wave resulted in continued changes as it related to choices in food purchasing and consumption. In 2022, IRI, 210 Analytics and the International Fresh Produce Association (IFPA) will continue to team up to document the ever-changing marketplace and its impact on fresh produce sales.

Meals remained home-centric in December. According to the IRI primary shopper survey, the share of meals prepared at home remained at 80%. The share of in-store versus online trips to buy groceries gained a little in December (86%) versus its November levels (83%) — perhaps related to holiday shopping.

During the early months of the pandemic, as many as 20% of trips were online. This dropped to a low of 11% in July of 2021.

Yet online shopping remains a complementary trip for most consumers. In December 2021, only 3% of survey respondents believe they will buy all their groceries online in the next month. This compares to 69% who believe they will buy everything in store, leaving 28% who will mix online and in-store grocery shopping. This signals a likely continuation of mixed format shopping for 2022 for a significant number of people. “Mixed format shopping is an important area to address for fresh produce,” added Parker. “Frozen and canned goods have very high online conversion but not everyone likes buying fresh produce online. Easing online buying hesitations will help build the online fresh produce basket as an important area of growth in 2022.”

Inflation

The consumer price index increased 6.8% for the 12 months ending November 2021, its highest since June 1982, according to the Bureau of Labor Statistics. IRI-measured price per unit for all food and beverages in multi-outlet stores, including supermarkets, club, mass, super-center, drug, military, and other retail food stores, also shows that prices continued to rise over and above their elevated 2020 levels. In December 2021, the average price per unit was up 8.3% versus December 2020 across all food and beverages. For the total year, prices increased 5.3% — pulled down by much milder inflation in the second quarter.

Source: IRI, Integrated Fresh Total US, MULO, inflation index vs. YAGO

Fresh produce prices are also higher than last year. In 2021, price per volume (pound) for total fresh produce increased by 6.5% — pulled down by much milder inflation early on in the year. When regarding inflation in December 2021 only, a comparison to 2020 shows a 14.7% increase for fresh fruit. December inflationary levels are much lower for vegetables, but still average +4.6%.

“Prices across the store and produce specifically are not only a concern for consumers,” said Joe Watson, VP, Retail, Foodservice & Wholesale for IFPA. “Inflation like this affects volume sales and we are a volume-driven business. Consumer efforts to save money typically start with buying what is on sale, but that is another area where we are struggling. Subsequent measures range from simply buying less to buying more frozen or canned, which all pressure volume.”

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. year ago.

2021 Sales

2021 brought $691 billion in food and beverage sales — up 1.8% over 2020 and 15.8% over the 2019 pre-pandemic normal. However, inflation played a significant role with year-on-year unit sales still down 3.3%. Perishables, including produce, seafood, meat, bakery and deli, had the highest year-over-year sales growth in 2021, at +2.2%. Frozen foods had the highest increase versus the pre-pandemic normal of 2019, at +23.0%. The performance by the produce department is right in line with the rest of the store. Year-on-year dollar gains were slightly above average, where the comparison to 2019 tracked slightly behind.

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. year ago.

From a dollar sales perspective, 2021 was another great year for fresh produce, surpassing the records set in 2020. However, dollar gains were inflation boosted and units and volume sales declined year-on-year. “Traditionally we have always compared our performance to the prior year and that is a hard habit to break,” said Watson. “But when we remove the unprecedented demand of 2020 and compare to the more typical levels of 2019, we see our true accomplishment. The fresh produce supply chain moved nearly 43 billion pounds through the registers in 2021, which was 7.1% more than 2019.”

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. year ago.

2021 Top Sellers Fruit and Vegetables

Source: IRI Integrated Fresh, Total U.S., MULO

The top sellers in 2021 reflect a mix of fruits and vegetables. Berry sales were nearly twice that of the number two, apples and tomatoes were the biggest seller on the vegetable side. Additionally, berries recorded the highest growth rates among the top 10 sellers, at +11.7%. Other areas with high year-on-year growth were salad kits and melons.

Not all top 10 sellers grew sales in 2021. Tomatoes, potatoes and peppers lost a little ground compared with their 2020 records.