Eight months into the pandemic, the virus remains in firm control of how and where people spend their food dollar.

Everyday sales have been on a slow march back to normal and restaurant transactions had come within 10% of prior year levels. Come September, many of the pandemic shopping patterns had started to normalize, including comfort levels with being in-store and the time consumers spent browsing for old favorites and new items.

During October, COVID-19 cases started to rise once more. This challenged further restaurant sales recovery, in combination with outdoor seating capacity being affected by colder temperatures in Northern states.

As a result, dollars at retail continued to pace well ahead of 2019 levels during the month of October, at +8.6% for total edibles.

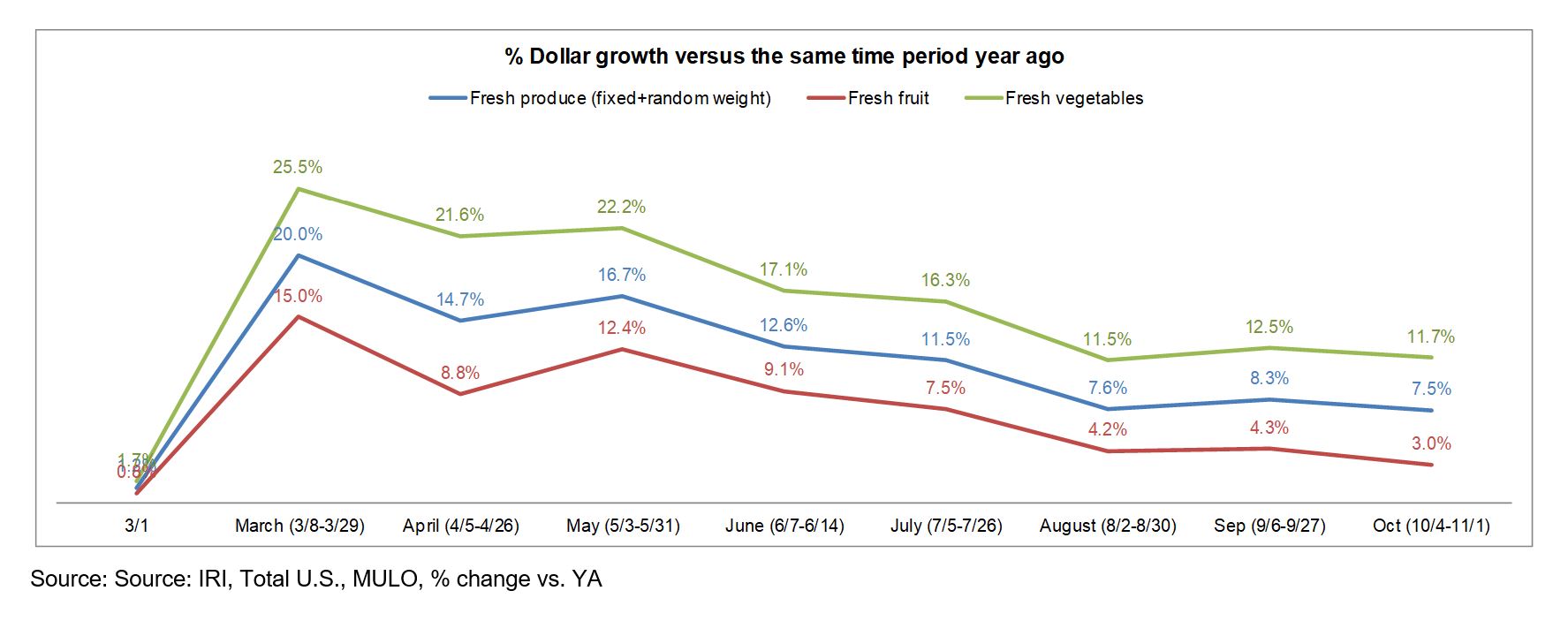

Food spending at retail remained highly elevated for all temperature zones of produce as well. Frozen fruit and vegetable sales are the smallest, but did see above-average gains. Fresh produce was up 7.5% during the October weeks and 10.0% for year-to-date.

“We all remember the days we looked closely at the decimal when studying growth percentages,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA).

“To see that produce sales are up 10% year-over-year ten months into 2020 is very telling. At-home consumption remains elevated across meal occasions, particularly among families with children who are in virtual schooling or people working from home. Our opportunity is to support consumers with meal planning and preparation during everyday and holiday weeks in the months to come to help them integrate fresh produce across meal occasions.”

Fresh produce generated $4.86 billion in sales during the October weeks — an additional $339 million in sales versus the same time period in 2019. This encompasses $64 million in additional fruit sales and $278 million in additional vegetable sales. Vegetable sales have outpaced fruit sales throughout the pandemic and have generated 34 weeks of double-digit growth since the onset of the pandemic shopping patterns in mid-March.

Fresh Share

Fresh produce commanded an 81.4% share of total fruit and vegetable sales across all three temperature zones during the October weeks — up a percentage point from its September average of 80.3%. “The fresh share moves up and down a bit depending on the month, but remains down compared with the 2019 level of 84% of sales,” said Jonna Parker, Team Lead for Fresh at IRI.

“Consumers still want to have multiple weeks’ worth of food in their freezers, fridges and pantries. In our most recent shopper survey in October, more than three-quarters aimed to buy enough to have one to two weeks worth of groceries and 15% aimed to buy three to four weeks worth. This desire to have backup will likely lead to continued strong sales of frozen and shelf-stable fruits and vegetables in addition to fresh gains.”

Fresh Produce Dollars versus Volume

Until May, fresh produce volume gains outpaced dollar gains. That flipped come June and for three months dollar gains outpaced volume gains, which is a sign of inflation.

September saw a reversal yet again, with volume up 9.2% and dollars 8.3%, which was driven by aggressive prices during Labor Day in particular. In the weeks ending October 4 through November 1, dollar gains once more exceeded volume gains, at +7.5% versus 6.1%.

“Volume at retail was up 6.1% in October versus year ago,” said Watson. “This is down a bit from September that included the Labor Day holiday sales, but up from August. With all the indicators pointing to more of the dollars flowing back into retail, it is likely that we will see a stronger November.”

In vegetables, dollar gains easily exceeded volume gains in October 2020 versus year ago. In fruit, it was the reverse, with a modest increase of 4.3% in volume and 3.0% in dollars. This continues the trend seen in September, when fruit volume gains exceeded dollars for the first time in months.

Absolute Dollar Gains

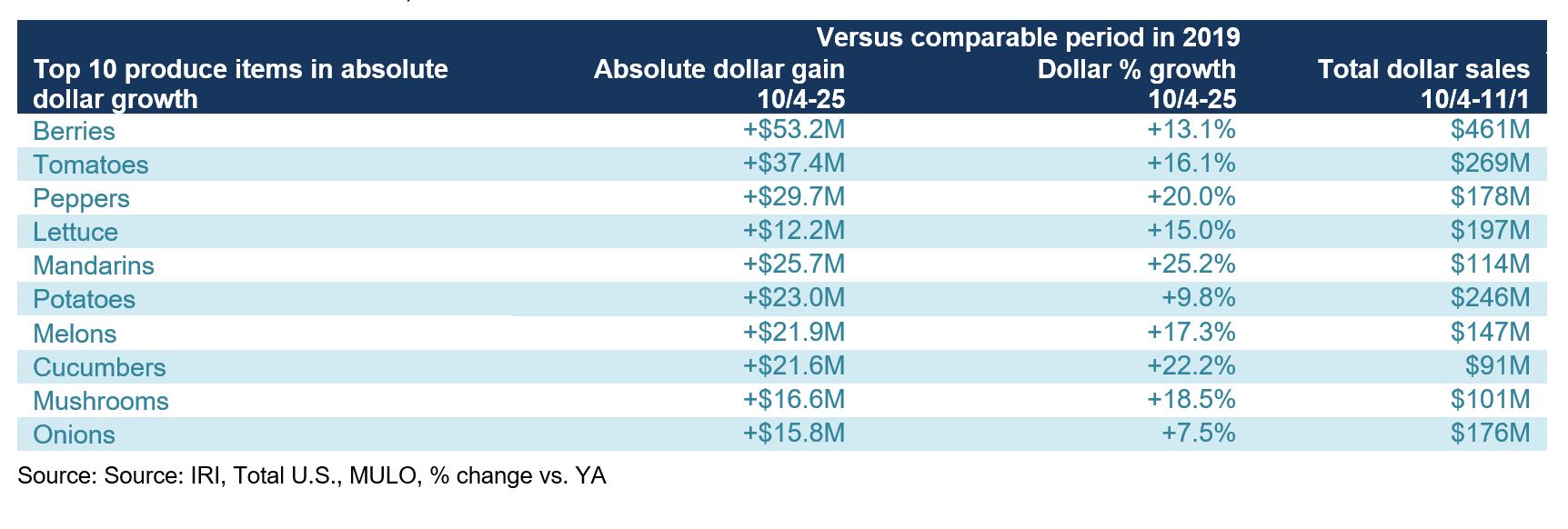

“Further reinforcing the strength of vegetables amid the pandemic are seven appearances in the Top 10 in absolute dollar gains for October 2020 versus year ago,” said Watson. “That said, the number one area in terms of adding new dollars was once more berries, with an additional $53.2 million in sales versus October 2019.”

Fresh Fruit

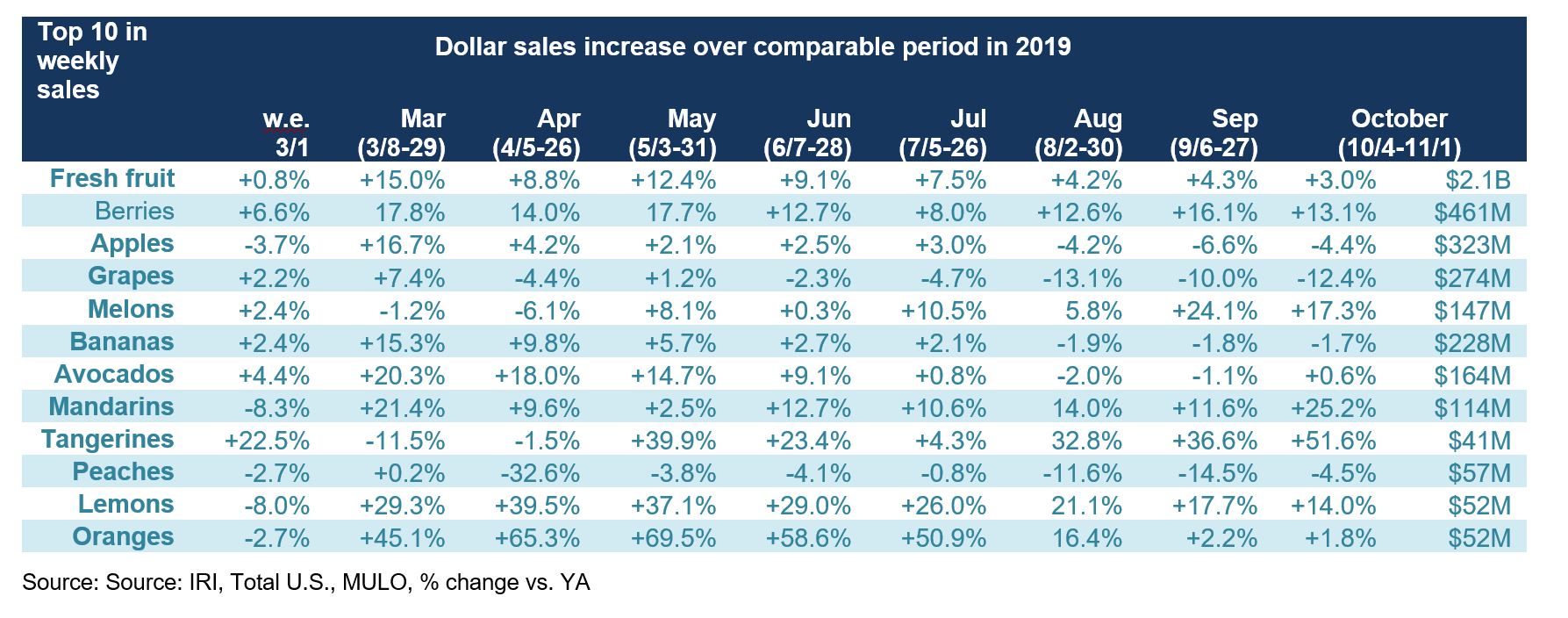

“In fruit, berries remained dominant in sales but you can see fall has arrived with strong apple and grape sales,” said Parker. “Not all top 10 areas gained in sales, in fact grapes, bananas and peaches lost some ground versus year ago. But on the other hand, berries, melons, mandarins, tangerines and lemons still up double-digits gains in October 2020 versus the same time period in 2019.”

Fresh Vegetables

The top 10 in sales on the vegetable side included eight items that had double-digit increases versus year ago and none that lost ground. “Comparing the strength of the top 10 players in vegetables to the more mixed performance in fruit shows why fresh vegetables have been a pandemic powerhouse,” said Watson.

“Tomatoes, potatoes, lettuce, peppers, onions, mushrooms and more are all meal ingredients, predominantly in dinner and lunch. Their continued strength underscores Americans are still eating more meals at home. At the same time, tomatoes, peppers and cucumbers have done a terrific job in merchandising against the snack meal occasion and clearly that is paying off in big year-over-year sales gains.”

Fresh versus Frozen and Shelf-Stable Fruits and Vegetables

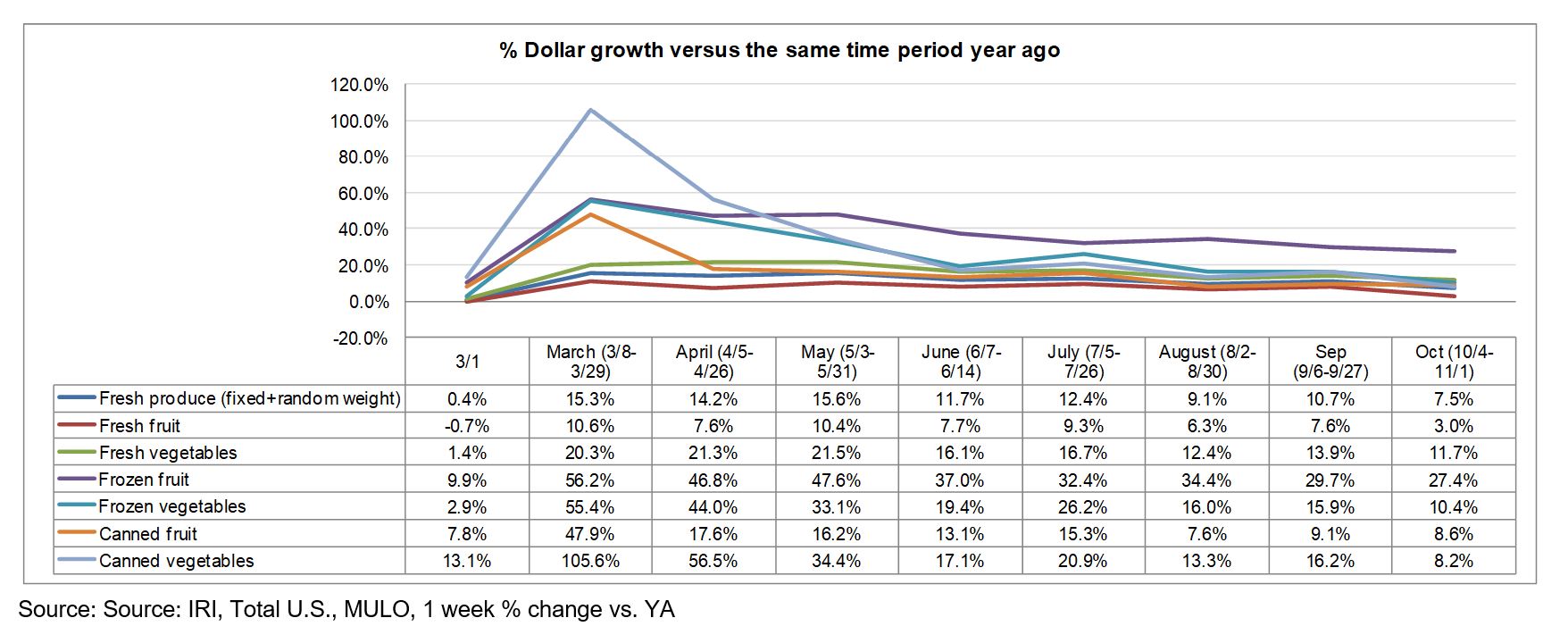

October brought gains for fruit and vegetables across all temperature zones. The highest percentage gains were reserved for frozen fruit. However, this is also the smallest of sales areas.

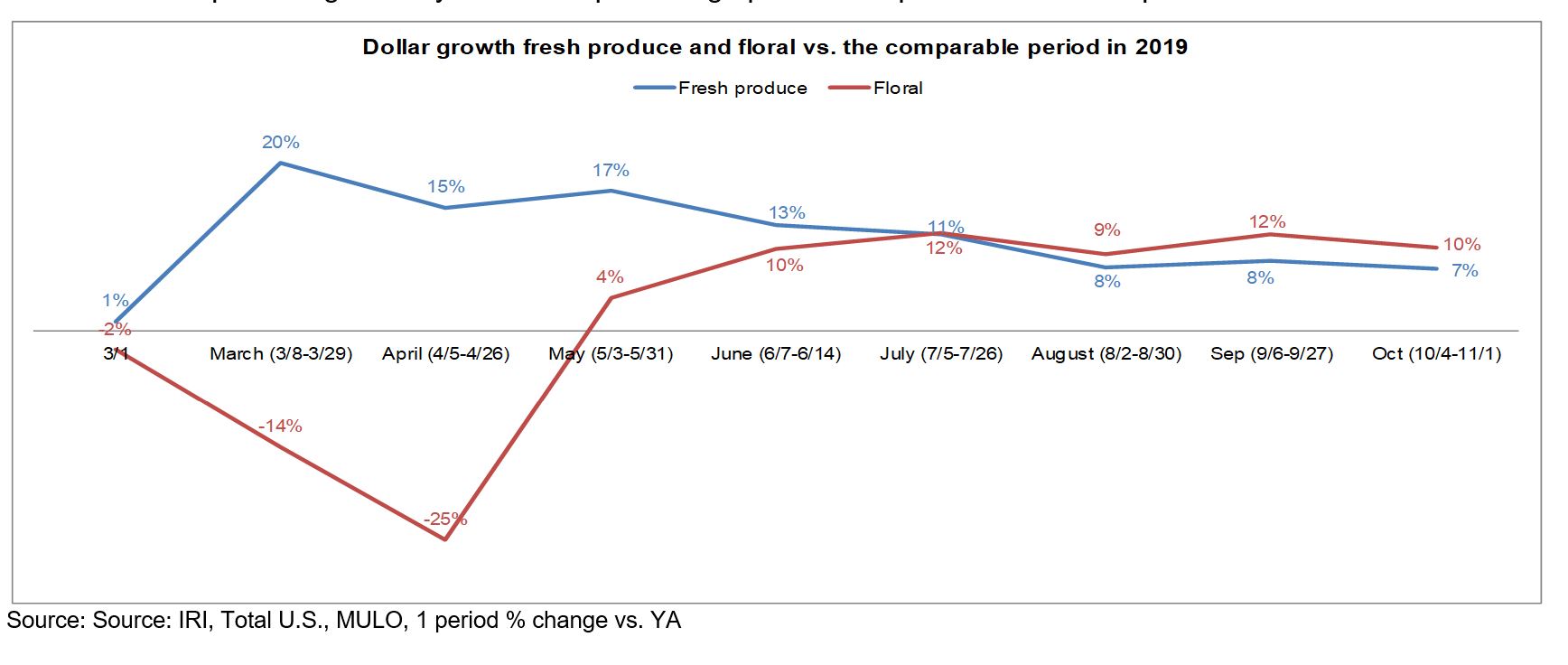

Floral

Floral struggled early on in the pandemic as retailers focused on keeping the produce department stocked, but has been trending well above year ago levels ever since May. After two months of near identical gains, floral sales gains actually exceeded fresh produce growth by about four percentage points in September and three points in October.

Perimeter Performance

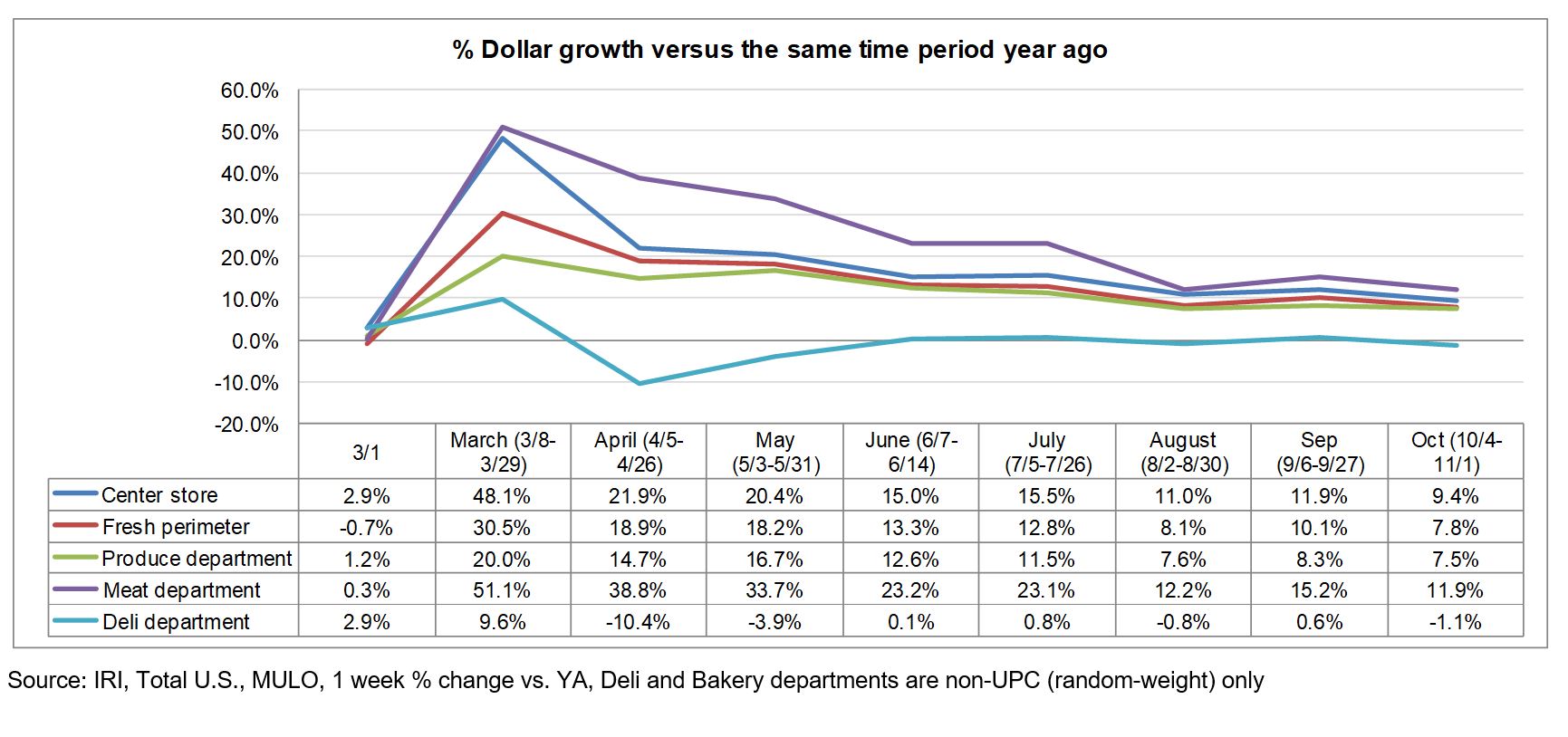

A look across departments shows that the meat department was the only one to exceed total center store grocery. Meat sales were up 11.9% over October. The deli department continued to sit right around year ago levels, sometimes slightly ahead, sometimes slightly behind. Deli meat and cheese sales were well ahead of last year, but deli-prepared continued to be an area of struggle.

What’s Next?

Everyday demand continues to hold around 12% for fresh vegetables and single digits for fresh fruit above year ago levels. As COVID-19 case counts continue to rise throughout the country, renewed shelter-in-place restrictions are likely to push dollars to food retail once more.

However, the sales surges may be more regionalized based on COVID-19 restrictions and cases. Aided by the effect of online sales, trip reduction, virtual schooling and working-from-home, produce sales are likely to remain well above 2019 levels for many weeks to come. However, holiday demand is likely going to be very different.

According to the latest weekly shopper survey wave by IRI, Thanksgiving will involve much less travel and smaller gatherings.

• Just over one-quarter of consumers, 26%, expect to host or attend a Thanksgiving meal with family who do not live with them, down sharply from 48% last year.

• Just 4% will travel out of state to attend a celebration, and only 19% of these people plan to fly.

• The median number of people at the main Thanksgiving meal is expected to be five this year, down from 8 last year.

• One-third expect to spend less on groceries for Thanksgiving this year, primarily due to hosting fewer/no guests this year or having to prepare a meal on a tighter budget.

These predictions point to many potential changes for the produce department. Some shoppers are predicting serving different meats or several smaller gatherings. This may result in different fruits and vegetable choices.

Much like the pandemic-affected holidays to date, grower/shippers and retailers may consider messaging and promotions that help shoppers find new ways to make the holidays special at home or on a tighter budget, and retailers should plan for an earlier spike in holiday item purchasing than last year. One in five people plan to shop more than three days earlier than last year, either to avoid crowds or out-of-stocks.

The next report, covering October, will be released in mid November. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.